This study assessed the financial knowledge, attitudes, behaviors, and overall literacy of Business Administration students at St. Rita’s College of Balingasag, Inc. A descriptive research design was employed, involving 110 students across year levels who completed a validated questionnaire adapted from Fessler et al. (2020). The instrument assessed students’ knowledge of financial concepts, their attitudes toward saving, spending, borrowing, and investing, as well as their corresponding financial practices. Findings revealed that while most students demonstrated developing financial knowledge, none achieved advanced proficiency, particularly in complex areas such as investments and debt management. Students exhibited strong pro-saving attitudes and confidence in managing personal finances, yet misconceptions about loans and limited familiarity with formal financial systems persisted. In terms of behavior, students consistently practice expense tracking and goal setting, although the majority relied on informal saving methods, such as keeping cash at home. The findings highlight a gap between students’ theoretical knowledge and its practical application. To address this, the study recommends curriculum enhancements and targeted interventions that promote responsible borrowing, strengthen investment literacy, and encourage the adoption of secure financial tools. These results provide a valuable baseline for developing financial literacy programs that aim at equipping students with essential competencies for both personal and professional decision-making.

Financial literacy is the ability to understand and apply financial skills effectively, including budgeting, saving, investing, borrowing, and managing debt 1. It allows individuals to make informed financial decisions, avoid unnecessary debt, and plan for long-term financial security. Research has reliably shown that individuals with higher financial literacy are more likely to show responsible financial behaviors such as saving for emergencies, planning for retirement, and using credit wisely 2. This concern is especially relevant for Business Administration students, who are expected to apply financial principles in both their academic and future professional lives.

Financial literacy encompasses several interrelated dimensions—namely, financial knowledge, financial attitude, and financial behavior. Financial knowledge encompasses both a substantive understanding of financial systems, such as how markets operate, and the practical ability to make informed decisions, including comparing the cost and quality of goods and services 3. Beyond factual knowledge, financial attitude reflects an individual’s mindset toward financial matters, emphasizing the importance of creating and sustaining value through sound decision-making and effective resource management 4. Meanwhile, financial behavior refers to the actual practices and actions individuals take in managing their finances, including budgeting, saving, spending, and handling debt. This behavior is shaped by a range of factors, including personal upbringing, cultural background, income, education, and life experiences 5. Together, these dimensions provide a comprehensive view of a person’s financial capability and readiness to make responsible financial decisions.

In Southeast Asia, financial literacy levels are also alarmingly low. The World Economic Forum’s 2021 report revealed that financial literacy in the region is among the lowest globally, with only 24% of Vietnamese adults considered financially literate. Other countries in the region, including the Philippines (25%), Cambodia (18%), Indonesia (32%), and Thailand (27%), show similarly concerning rates 6, 7. However, even among Business Administration students who are academically exposed to financial topics, there remains a gap in practical financial understanding and behavior 8. Many still struggle with basic financial concepts such as compound interest, risk diversification, and effective debt management. Addressing all three dimensions is vital in designing effective interventions that prepare students for sound financial decision-making and long-term financial well-being 9.

While prior studies have established general low financial literacy in the Philippines, focused research is scarce on the specific interplay of knowledge, attitudes, and behaviors among Business Administration students in private higher education institutions in Northern Mindanao. This study seeks to fill this gap by providing a granular, descriptive analysis of these three dimensions among students at St. Rita’s College of Balingasag, Inc. Specifically, it seeks to describe the students’ understanding of financial concepts, examine their attitudes toward saving, spending, borrowing, and investing, and identify their common financial behaviors and practices. In addition, the study aims to explore potential patterns and trends in financial decision-making across variables such as year level, gender, and socio-economic background. Ultimately, the findings are intended to serve as baseline data that may inform and guide the development of future financial literacy programs or interventions within the institution.

General Objective of the Study

This study aims to assess the level of financial knowledge, attitude, behavior, and literacy of Business Administration Students in a Private Higher Education institution. Specifically, the study aims to describe their financial knowledge, identify patterns and trends in the financial attitude, behavior, and decision-making processes of Business Administration students. Further, this study aims to provide baseline data that may serve as a reference for future financial literacy programs or interventions within the institution.

Research Questions

1. What is the level of financial knowledge among Business Administration students in a private higher education institution?

2. What are the financial attitudes of Business Administration students toward saving, spending, borrowing, and investing?

3. What are the common financial behaviors and practices of Business Administration students?

In this study, a Descriptive research design is utilized. Descriptive research design is a fundamental approach in observational studies that aims to describe and characterize a population or phenomenon without testing causal relationships 10. In this study, a descriptive research design was used to describe the level of financial knowledge, attitude, behavior, and literacy of Business Administration Students in a Private Higher Education institution.

2.2. Setting and ParticipantsThe study is conducted at St. Rita’s College of Balingasag, Inc. – a private higher education institution in the Philippines. The participants of this study were the currently enrolled Financial Management Students under the Bachelor of Science in Business Administration Program from the 2nd year to the 4th year levels during the academic year 2024- 2025.

2.3. Research InstrumentThe survey instrument of this study is adapted from 11. [Cronbach’s α = 0.8]. This instrument assesses the financial knowledge, financial attitudes, and financial behavior. The questionnaire is divided into three sections, each targeting a key component of the study: Section A consists of five multiple-choice questions that measure the respondent’s understanding of basic financial knowledge. These questions covered the domains of compound interest calculation, inflation, risk diversification, basic debt management, and financial product functionality. A correct answer to all questions was required to be classified as ‘Advanced’ knowledge. Section B assesses students’ personal beliefs, preferences, and perspectives regarding money management. It includes five statements rated on a 5-point Likert scale ranging from 1 (Strongly Disagree) to 5 (Strongly Agree). And Section C evaluates the respondents’ actual financial practices. It consists of five multiple-choice questions that provide insight into the students’ real-life application of financial skills and knowledge.

2.4. Data Gathering ProcedureThe study involved 2nd to 4th year Financial Management students at St. Rita’s College of Balingasag, Inc., using total population sampling. Prior approval from the Program Head, Dean, and Research Office is secured, and coordination with instructors helps schedule survey administration. A validated questionnaire was distributed in digital form using Google Forms, with informed consent obtained from all participants. Students were given 15–20 minutes to complete the survey. Collected data were checked, encoded, and analyzed using descriptive statistics—mean, frequency, and standard deviation—to assess financial knowledge, attitudes, and behaviors.

2.5. Statistical AnalysisThe measures of central tendency were utilized for analyzing the collected data. This includes mean, frequency, and standard deviation. For Section A, frequency and percentage distributions were used to determine the variability of students’ financial knowledge. For Section B, each statement rated on a five-point Likert scale was analyzed using the mean to identify the general tendency of student attitudes, and the standard deviation measured the extent of variation. For Section C, frequency count and percentages summarized students’ self-reported financial practices.

The data reveal a significant competency gap. The vast majority of students were classified at a developing level, while none demonstrated advanced proficiency. This indicates that while students have grasped foundational financial concepts, they lack mastery in complex areas such as investment strategies, risk diversification, and advanced debt management. This finding is consistent with regional trends; the Philippines has a financial literacy rate of only 25% (Klapper & Lusardi, 2020; Maicle, 2025). For Business Administration students who are expected to apply financial principles professionally, this absence of advanced knowledge highlights a critical disconnect between academic exposure and practical mastery. It suggests the current curriculum may emphasize theoretical knowledge over its application, limiting students’ ability to navigate real-world financial decisions 8. As Lusardi & Messy (2023) note, advanced financial literacy is crucial for making savvy decisions and effectively using financial instruments.

3.2. What are the Financial Attitudes of Business Administration Students Toward Saving, Spending, Borrowing, and Investing?Students exhibited strongly positive attitudes toward saving and financial self-efficacy, with high levels of agreement on the importance of saving (Mean=4.80), and confidence in managing their finances (Mean=4.27). They also strongly supported the integration of financial literacy into the curriculum (Mean=4.50), recognizing its value. This pro-saving mindset aligns with cultural values of frugality observed in Southeast Asia (Adiputra & Patricia, 2020).

However, a critical attitudinal gap was identified concerning debt. Students held a neutral stance (Mean=2.90) on the statement “Taking loans is always a bad decision,” indicating a misconception about credit and a lack of understanding of responsible borrowing as a potential financial tool. This aversion may stem from cultural or familial skepticism towards debt, a common trait in regions with lower financial literacy (Bhushan & Medury, 2014). This finding reveals a paradox: high confidence coexisting with significant knowledge gaps, which could lead to overconfidence in financial decision-making.

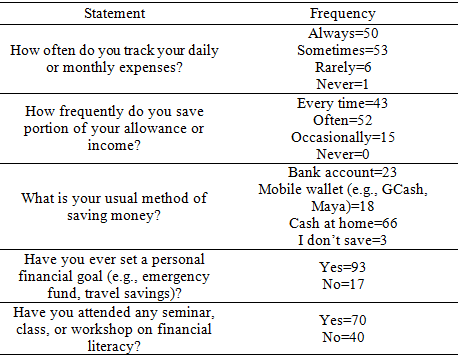

3.3. What are the Common Financial Behaviors and Practices of Business Administration Students?The data on financial practices reveals a strong foundation in financial discipline but a significant gap in the use of formal financial systems. A high percentage of students reported positive financial habits: 93.6% track their expenses at least sometimes, 86.4% save a portion of their income regularly, and 84.5% have set personal financial goals. This aligns with the finding that financial knowledge and attitudes from the intention for sound financial behavior 14.

The most striking finding, however, is that 60% of respondents primarily save money as “cash at home.” Only 37.3% use formal financial tools like bank accounts (20.9%) or mobile wallets (16.4%). This behavior reflects a distrust of or limited access to formal financial systems, mirroring the cash-heavy nature of the Philippine economy 13. While keeping cash may seem prudent, it exposes students to risk and prevents them from benefiting from interest earnings, secure transactions, and building a credit history.

Furthermore, although 63.6% had attended a financial workshop, this exposure did not translate into advanced knowledge or improved financial practices. This suggests that existing programs may be effective at raising awareness but are insufficient for fostering deeper competency and behavior change.

3.4. SynthesisThe study reveals a nuanced financial literacy profile among Business Administration students, characterized by a clear disconnect between knowledge, attitudes, and behavior: a knowledge gap where developing – but not advanced – proficiency limits complex decision-making; and attitudinal gap where debt misconceptions undermine high confidence and pro-saving intentions; and a behavioral gap where strong saving habits are negated by reliance on insecure cash savings. This triad of gaps indicates that positive financial intentions are thwarted by insufficient expertise and systemic barriers, affirming that financial literacy is multidimensional – excelling in one area cannot compensate for deficiencies in others (Lusardi & Mitchell, 2014). Thus, effective interventions must simultaneously address knowledge, attitudes, and behavior to translate intention into practice.

• 89.1% of students have developing financial knowledge.

• 0% demonstrate advanced understanding of complex topics such as investments and loans.

4.2. Confident but Misinformed Attitudes• Strong agreement on saving importance but a neutral stance on loans.

• High self-confidence despite knowledge gaps.

4.3. Behavior-Context Mismatch• 93.6% track expenses, but 60% save in cash, not banks or mobile wallets.

• 84.5% set goals yet lack tools to optimize savings.

The study reveals a critical disconnect between students’ positive financial intentions and their actual financial competencies and practices, highlighting three key areas for educational reform. First, the predominance of basic financial knowledge with no advanced mastery calls for curriculum enhancements, including practical modules on investment simulations, loan management case studies, and digital banking applications to bridge theory-practice gaps. Second, while students demonstrate strong saving intentions, their reliance on informal cash savings and misconceptions about credit underscore the need for myth-busting workshops and institutional partnerships with banks to promote secure financial tools and responsible borrowing practices. Third, the limited effectiveness of current financial literacy initiatives suggests transitioning from awareness-based training to competency-focused programs featuring hands-on budgeting exercises, post-workshop assessments, and real-world financial challenges. By implementing the integrated framework proposed by Lusardi and Mitchell (2014), which concurrently targets knowledge acquisition, attitudinal restructuring, and behavioral modification, educators can develop pedagogies that align with local financial ecosystems. This approach enables the cultivation of both technical proficiency and conceptual adaptability necessary for sustained financial competence. This holistic approach would transform classroom learning into actionable financial proficiency that aligns with professional demands and personal finance realities.

This study assessed the financial literacy of Business Administration students, revealing a profile of developed intentions undermined by underdeveloped competencies. The triad of findings – a significant advanced knowledge deficit, confident yet misinformed attitudes toward debt, and disciplined but informal financial behaviors – paints a clear picture of students who are motivated but inadequately equipped for complex financial decision-making. These findings underscore the multidimensional nature of financial literacy and highlight the inadequacy of one-dimensional educational approaches. Rather than confirming generalized low financial literacy, this research offers institution-specific, actionable insights that can inform curriculum design, pedagogical strategies, and institutional interventions. Moving forward, these results advocate for integrated financial education that combines theoretical instruction with practical application, including simulations of investment and debt scenarios, training in digital financial tools, and workshops addressing common misconceptions. By aligning educational content with the nuanced financial realities and behavioral patterns of students, institutions can better equip future business professionals with the competencies necessary for both personal financial resilience and professional success. This study thus serves as a foundational reference for designing targeted financial literacy programs that are responsive to the specific needs of learners in emerging economy contexts.

| [1] | Lusardi, A., & Mitchell, O. S. (2014). The economic importance of financial literacy: Theory and evidence. Journal of Economic Literature, 52(1), 5–44. | ||

| In article | View Article PubMed | ||

| [2] | Fernandes, D., Lynch, J. G., Jr., & Netemeyer, R. G. (2014). Financial literacy, financial education, and downstream financial behaviors. Management Science, 60(8), 1861–1883. | ||

| In article | View Article | ||

| [3] | Clark, G.L. (2020). Financial Knowledge. International Encyclopedia of Human Geography. | ||

| In article | View Article | ||

| [4] | Adiputra, I. G., & Patricia, E. (2020, May). The effect of financial attitude, financial knowledge, and income on financial management behavior. In Tarumanagara International Conference on the Applications of Social Sciences and Humanities (TICASH 2019) (pp. 107-112). Atlantis Press. | ||

| In article | View Article | ||

| [5] | Subburayan, B. (2023). Financial Behavioural of Individual’s Life. The Times of India, 0971-8257. | ||

| In article | View Article | ||

| [6] | Klapper, L., & Lusardi, A. (2020). Financial literacy and financial resilience: Evidence from around the world. Financial Management, 49(3), 589-614. | ||

| In article | View Article | ||

| [7] | Maicle, J.B. (2025). Assessment of financial knowledge among graduating university students. International Journal of Academe and Industry Research, 6(2), 55-77. | ||

| In article | View Article | ||

| [8] | Mandell, L., & Klein, L. S. (2009). The impact of financial literacy education on subsequent financial behavior. Journal of Financial Counseling and Planning, 20(1), 15–24. | ||

| In article | |||

| [9] | Bhushan, P., & Medury, Y. (2014). An empirical analysis of inter linkages between financial attitudes, financial behaviour and financial knowledge of salaried individuals. Indian Journal of Commerce and Management Studies, 5(3), 58-64. | ||

| In article | |||

| [10] | Aggarwal, R., & Ranganathan, P. (2019). Study designs: Part 2 – Descriptive studies. Perspectives in Clinical Research, 10, 34 - 36. | ||

| In article | View Article | ||

| [11] | Fessler, P., Silgoner, M., & Weber, R. (2020). Financial knowledge, attitude and behavior: evidence from the Austrian Survey of Financial Literacy. Empirica, 47(4), 929-947. | ||

| In article | View Article | ||

| [12] | Lusardi, A., & Messy, F. A. (2023). The importance of financial literacy and its impact on financial wellbeing. Journal of Financial Literacy and Wellbeing, 1(1), 1-11. | ||

| In article | View Article | ||

| [13] | Jonveaux, B. (2024). Philippines–Preserving economic stability, financing development and anticipating climate issues. AFD MacroDev, (54), 1-12. | ||

| In article | |||

| [14] | Coskun, A., & Dalziel, N. (2020). Mediation effect of financial attitude on financial knowledge and financial behavior: The case of university students. International Journal of Research in Business and Social Science, 9(2), 1-8. | ||

| In article | View Article | ||

Published with license by Science and Education Publishing, Copyright © 2025 Katrina C. Japona, Josua U. Cabural, Jose D. Escalera and Katrina C. Japona

![]() This work is licensed under a Creative Commons Attribution 4.0 International License. To view a copy of this license, visit

http://creativecommons.org/licenses/by/4.0/

This work is licensed under a Creative Commons Attribution 4.0 International License. To view a copy of this license, visit

http://creativecommons.org/licenses/by/4.0/

| [1] | Lusardi, A., & Mitchell, O. S. (2014). The economic importance of financial literacy: Theory and evidence. Journal of Economic Literature, 52(1), 5–44. | ||

| In article | View Article PubMed | ||

| [2] | Fernandes, D., Lynch, J. G., Jr., & Netemeyer, R. G. (2014). Financial literacy, financial education, and downstream financial behaviors. Management Science, 60(8), 1861–1883. | ||

| In article | View Article | ||

| [3] | Clark, G.L. (2020). Financial Knowledge. International Encyclopedia of Human Geography. | ||

| In article | View Article | ||

| [4] | Adiputra, I. G., & Patricia, E. (2020, May). The effect of financial attitude, financial knowledge, and income on financial management behavior. In Tarumanagara International Conference on the Applications of Social Sciences and Humanities (TICASH 2019) (pp. 107-112). Atlantis Press. | ||

| In article | View Article | ||

| [5] | Subburayan, B. (2023). Financial Behavioural of Individual’s Life. The Times of India, 0971-8257. | ||

| In article | View Article | ||

| [6] | Klapper, L., & Lusardi, A. (2020). Financial literacy and financial resilience: Evidence from around the world. Financial Management, 49(3), 589-614. | ||

| In article | View Article | ||

| [7] | Maicle, J.B. (2025). Assessment of financial knowledge among graduating university students. International Journal of Academe and Industry Research, 6(2), 55-77. | ||

| In article | View Article | ||

| [8] | Mandell, L., & Klein, L. S. (2009). The impact of financial literacy education on subsequent financial behavior. Journal of Financial Counseling and Planning, 20(1), 15–24. | ||

| In article | |||

| [9] | Bhushan, P., & Medury, Y. (2014). An empirical analysis of inter linkages between financial attitudes, financial behaviour and financial knowledge of salaried individuals. Indian Journal of Commerce and Management Studies, 5(3), 58-64. | ||

| In article | |||

| [10] | Aggarwal, R., & Ranganathan, P. (2019). Study designs: Part 2 – Descriptive studies. Perspectives in Clinical Research, 10, 34 - 36. | ||

| In article | View Article | ||

| [11] | Fessler, P., Silgoner, M., & Weber, R. (2020). Financial knowledge, attitude and behavior: evidence from the Austrian Survey of Financial Literacy. Empirica, 47(4), 929-947. | ||

| In article | View Article | ||

| [12] | Lusardi, A., & Messy, F. A. (2023). The importance of financial literacy and its impact on financial wellbeing. Journal of Financial Literacy and Wellbeing, 1(1), 1-11. | ||

| In article | View Article | ||

| [13] | Jonveaux, B. (2024). Philippines–Preserving economic stability, financing development and anticipating climate issues. AFD MacroDev, (54), 1-12. | ||

| In article | |||

| [14] | Coskun, A., & Dalziel, N. (2020). Mediation effect of financial attitude on financial knowledge and financial behavior: The case of university students. International Journal of Research in Business and Social Science, 9(2), 1-8. | ||

| In article | View Article | ||