The ECGCL (Economic Community of the Great lakes countries) and its member states, like most low-income countries, have a very large public external debt and a weakness in terms of investment. Hence the question of asking “What impact can the public debt have on public and private investment.”? To carry out this study, two models were specified on the basis of the existing theoretical and empirical literature and according to the specificities of the economy of the ECGCL and its member countries. After preliminary tests (individual effects tests and Hausman specification test) which led to private investment estimation through the Folly-modified Ordinary Least Square and Ordinary Least Square ; and to public investment estimation by the Generalized Least Square, it appears from this study, that public investment positively impacts private investment and vice versa, the government-backed stock of public debt, on the other hand, has a negative impact on private investment, contrary to its positive relationship with the public investment. As for the servicing of the public debt and guaranteed by the State, it negatively influences the investment (public and private long-term).

Increased public spending, insufficient domestic savings and reduced sources of the tax base explain the use of borrowing. It followed the tremendous increase in public debt that began in the late 1960s and led to a crisis of repayment from 1982{1}. The public debt of the Third World countries was thus multiplied by twelve between 1968 and 1980 1.

In addition, states have the obligation to resort to the financial markets or their citizens to make up for any budget deficit and can’t borrow at zero rate. Against the high interest rates of the debts, the States must give pledges of "good management" to the financial markets by restraining the public expenditure which can have in general repercussions on the level of the public investments and consequently on the level private 2.

It is obvious that following the first oil shock, a double laxity intervened. On the side of the creditors who first, having to face the recycling of euro dollars, then petrodollars{2}, have developed a lending business to the Third World countries. In the case of developing countries afterwards, the credits obtained have scarcely been used rationally. Instead of financing productive investments, the only ones likely to strengthen the export capacity of these countries and generate the foreign exchange flows needed to repay the debt, the governments of the indebted countries have embarked on more profitable investment programs questionable and too often unsuited to local needs 3.

Thus, over the last three decades, the economic context has been marked by massive indebtedness for many developing countries 8. In recognition of the fact that the debt of the poor countries had become unsustainable and undermined their development, in 1996 the donor community launched the Heavily Indebted Poor Countries Initiative, which resulted in cancellation of the external debt of certain developing countries, including those of the ECGLC. These cancellations associated with Structural Adjustment Programs (SAPs) have mitigated short-term liquidity problems related to debt service, but in the long run they have generally experienced mixed results. Worse debt burden is still heavy and continues to grow, so that some countries have come to a debt they can’t serve today 4.

Thus, the debate on the effects of public debt is now attracting more attention, especially as many countries continue to engage in processes of state debt reform. Governments and the international financial community face an unfavorable environment in the process of economic and social development following the scourge of indebtedness 5.

The problem of public debt in macroeconomic theory arises from the effects of the State's debt on the real economy in general and more particularly on investment 6. Since Barro's analyzes, economists have constantly revised their exhausted initial beliefs in Keynesian and neoclassical theories. For the classics the interventionism of the State is a source of market imbalance due to the effects of evictions linked to the increase of the public debt and the interest charge while for the Keynesians, the State must play a key role in the process of economic growth through public spending and especially public investment 7.

The debate on the impact of the public debt on investment (public and private) has therefore in recent years been considerable in both the importance of its implications in terms of economic policy and the number of theoretical analyzes; and empirical to which it gave rise 8. In most empirical studies, a reduced form of investment or growth equation is used, under which the stock of debt is assumed to affect it either directly or indirectly. Some authors like 7 concluded that the debt crisis did not depress the investment. However, others like 9, 10, as well as 11 found results in favor of the virtual debt burden hypothesis. In addition, many other studies have demonstrated the effect of public investment on private investment. The conclusions differ as to the nature of this impact. Some authors like 9 as well as 12 have resulted in a long-term complementarity relationship, while others such as 8 and 13 have confirmed the hypothesis of the eviction effect.

The reference 14 has illustrated the external debt relationship, public investment and growth in fifty-five low income countries, and resulted in the following findings that high stock of external debt can depress economic growth in low-income countries through its effects on efficient use of resources rather than depressing private investment. In addition, external debt also affects growth through an indirect effect through public investment. However, the stock of public debt does not seem to depress public investment. For these authors, reducing the debt of low income countries will have a positive impact on their economic growth. So if half of the debt service is channeled, without increasing the budget deficit, then growth could accelerate by 0.5 point per year.

On the other hand, there are few empirical arguments for developing countries on the question of the impact of public investment on private investment, and several studies have confirmed the idea that the effect depends on the degree of complementarity or substitutability between public investment and private investment. The reference 9 determined the relationship between indebtedness and private wealth accumulation in 23 countries over the period 1975-1987, interpreted the relationship between public investment and private investment as long-term complementarity and short-term substitutability.

Compared to other works that we have used, ours presents peculiarities in the sense that it wants to study the temporal aspects close to the current date by integrating in its analysis the last years that these other works n ' did not take it into account. The importance of the sample in the fact that the PANEL data will even be the key to this work is also necessary, especially since we will have to deal with a huge sample. What other authors have not done except for some reports of international organizations. In addition, the insufficiency of such studies for the ECGLC countries, will make our work a particularity in the sense that it is interested in a whole economic region of enormous importance in terms of economic potential, human, hospital, etc.

The problems of indebtedness and especially of the assignment of the latter are also very acute in Africa and mainly south of the Sahara 15. For this, throughout our work we will undertake a study that will address the impact of public debt on investment by bringing all our thinking on ECGLC member states.

Comparing the last two years for each ECGLC Member State, we observe the decrease in the stock of public debt related to Gross National Income{3}, the increase in the public debt service relating to exports in terms of these states' commitment to repaying the debt{4} as well as the decrease in the level of investments (public and private){5}. Based on these three observations, we note that in the three ECGLC member states, much more resources are devoted to debt repayment than to capital expenditures. The high level of this indicator (debt service) in relation to the evolution of the level of investment in the ECGLC member states is problematic even though we know that the objectives for sustainable development suggest to highly indebted poor countries. (HIPCs) to spend more than 35% of their GDP on investment with a view to achieving a 7% growth rate by 2020.

In view of all this, even though the governments of the ECGLC member states still tend to use borrowing to ensure a balanced budget and thus have the necessary means to finance public investments without trying to asphyxiate those of the private sector; a major concern is: What influences the change in the level of investment in ECGLC member states? From this overarching question, two other questions that merit particular attention deserve special attention: What is the impact of public investment on private investment in ECGLC member states? What is the impact of stocks and services of public external debt on investment in ECGLC member states?

Thus, supporting the studies of 16 and those 9, we say that domestic credit, the terms of trade, the real exchange rate, the public debt, interest, the rate of inflation, real GDP growth, external aid and population growth explain the variation in investment in the ECGLC member states. The same studies by 9 urge us to advance the idea that public investment has a long-term complementarity relationship and short-term substitutability for private investment in ECGLC member states. On the other hand, using the work of 13 as well as those of 14, we say that the stock and service of public external debt would negatively influence investment in Member States of the ECGLC.

The main objective of this study is to examine the effects of public debt on investment (public and private), without neglecting the other determinants of the latter. In addition to this objective, this work proposes in the institutional framework of ECGLC member states to describe the evolution and structure of certain macroeconomic indicators having influence on public or private investment and to identify possible links between them. It will also discuss the impact of public investment on private investment.

We chose this topic to deal with phenomena that hinder the economic performance of countries, namely: a huge and poorly negotiated public debt as well as poorly chosen and poorly managed public investment projects. In reality, each country undoubtedly presents specificities that make the weight of the debt not felt in the same way. Therefore, the analysis of the impact of public debt on the level of investments for a country is of major interest 4.

The study of the relationship between borrowing and investment is therefore of practical interest for a number of reasons: the persistence of fiscal deficits for ECGLC member countries, sometimes low annual growth rates due to shortcomings public and private investments. On the theoretical level, it is a question of highlighting two seemingly distant but closely related issues of question, namely public debt and investment. In terms of "operational" interest, the question is whether the public debt is virtuous, that is, how is it likely to turn into productive investment, a source of economic growth. The empirical determination of the impact of the public debt on investment would be likely to guide economic policy choices in the ECGLC member states.

These investigations are carried out within the space of the ECGLC member states, which is a community of three sovereign states: the Democratic Republic of Congo, the Republic of Burundi and the Republic of Rwanda. They focus on the time span from 1960 to 2015. Period during which the public debts have increased enormously in all countries including those of the ECGLC.

In addition to the introduction and the conclusion, our work is articulated around three points. The first point is devoted to the presentation of the material and methodological approach necessary to test our hypotheses. The results of our analyzes results and the different tests to be carried out will be presented in the second point. The third chapter is devoted to the discussion of the results.

Three approaches to the relationship between debt and investment can be distinguished:

- According to the first, external debt is considered as a return of capital with positive effects on domestic savings, investment and growth. Proponents of this argument assume that foreign savings are complementary to domestic savings;

- For 17, 18, who are the proponents of the second acceptance, if the future debt of a country tends to be higher than its repayment capacity, servicing its debt will be a growing function of its production, thus discouraging domestic and foreign investors. Fearing that production will be taxed by the state as debt servicing progresses, potential investors will be reluctant to bear immediate costs to increase future production. This is the thesis advanced by the authors of the theory of "over-indebtedness" or the "virtual burden of debt";

- Proponents of the third approach attempted to reconcile the two previous viewpoints by developing models with non-linear effects of debt on investment and growth 19.

After drawing theoretical lessons on the debt and investment relationship, we will expose those relating to the link public investment and private investment.

Because of the importance of public investment in developing countries, it is necessary to analyze its complementarity or substitutability with private investment. Theoretically, the accelerator effect and the crowding out effect of public investment on private investment can be taken into account. But a priori the net impact remains indeterminate.

For (International Monetary Fund, 1990), there is a positive impact between public investment and private investment, and this impact manifests itself when one particularly analyzes the share of public investment for infrastructure and not the total public investment. Thus, any increase in public investment also increases private investment because of the creation of new infrastructure that subsequently attracts private investors.

For 20 on the other hand, the idea of an effect of crowding out public investment has long prevailed in the elaboration of structural adjustment programs. However, the crowding out effect in developing countries does not manifest itself in the same way as in developed countries. It is quite likely that it will take one of three forms:

- First, the limited size of markets in most developing countries can mean that public investment in productive sectors exposes private firms, thus causing a real crowding out effect;

- Secondly, the final foreclosure effect can take place as if all agents are organizing to limit their credit pool;

- Third, public investment financing through its effects on inflation and debt accumulation can create uncertainty in the business environment 21. In contrast, endogenous growth models tend to revive the role of public investment modeled by BARRO in 1990.

2.2. Empirical ReviewAn abundant literature has established the possible existence of a link between the stock of external debt and private investment (virtual debt burden or debt overhang). In most studies, a reduced form of investment or growth equation is used, under which the stock of debt is assumed to affect it either directly or indirectly. In some countries, authors like 7 concluded that the debt crisis did not depress investment. However, others like 9, 10, 11, 22 found results in favor of the virtual burden hypothesis debt. This empirical review will be organized around two poles. A first cluster will bring together the few conceptions that public debt has a positive impact on investment and growth. The second pole will be devoted to authors who assume a negative effect of the debt.

For theories in favor of a positive impact of the debt 23, studying the behavior of investment in data from fifteen debtor countries during the period 1971-1987, concluded that public debt does not act on the pace and volume of investment private. In the model they used, the investment rate is a function of the debt ratio, the net transfers, the savings volume and the real interest rate and the previous level of investment. The estimation of this function has shown that the relation between the weight of the debt and the investment is not negative.

The results of 19 on the correlation between debt and private investment in developing countries in the 1980s, show that the high level of the stock of debt does not appear to have a very great power in the explanation the decline in investment.

The reference 24 finds for a sample of 54 developing countries (including 14 highly indebted countries) that the inclusion of three additional explanatory variables (fiscal balance, inflation and openness) leads to the rejection of statistical significance of the negative effect of external debt on investment and growth.

The reference 25 concluded in their work on Turkey that external indebtedness has had a positive effect on private investment during the import-substitution industrialization, and over-indebtedness failed to curb investments. According to these authors, this positive correlation between external debt and private investment is explained by the fact that the private sector has replaced the public sector as an external borrower.

There are also other studies showing favorable effects of the external debt, notably those of the 26 for the period 1980-1986 and 27 for Bangladesh, Indonesia and South Korea. After these few studies in favor of a positive impact of the external debt on investment and growth, we will develop the points of view of the authors who have found results verifying the hypothesis of the "virtual debt burden" and that of the "Laffer curve of debt".

For theories in favor of the “debt burdent” hypothesis, Several empirical studies have been developed to test the effects of disincentives and crowding out of the external debt burden on private investment in developing countries using ordinary least squares estimation methods. Most of these studies find one or more debt variables negatively significant and correlated with private investment.

This is the case of an IMF (International Monetary Fund) study (1989) 28 that assessed the investment behavior and growth rate of gross domestic production (GDP) in heavily indebted countries before and after the onset of the crisis of external debt. The investment-to-GDP ratio lost ten points from its 1975-79 level and seven points from 1980-81. This study concluded that the poor performance of investment in highly indebted economies with problems servicing their debt is related to the de-motivating effect of the debt burden.

The reference 9 examined the relationship between indebtedness and private accumulation in 23 countries over the period 1975-1987. They found that the coefficients of the two debt variables (the debt service ratio and the debt ratio measured by the ratio of debt stock to GDP) are negative and significant at 1%. Indebtedness would therefore have an unfavorable empirical effect on private investment. The authors have shown that the effects of debt on investment are more accentuated during the crisis period (1978-1982) than during the other two periods considered.

The reference 14 shows the relationship of external debt, public investment, and growth in fifty-five low-income countries, yielded the following results:

Ÿ The high stock of external debt can depress economic growth in low-income countries through its effects on the efficient use of resources rather than depressing private investment;

Ÿ External debt also affects growth indirectly through public investment. However, the stock of public debt does not seem to depress public investment;

Ÿ They believe that debt negatively affects growth beyond a threshold of 50% of GDP.

For these authors, reducing the debt of low-income countries will have a positive impact on their economic growth. So if half of the debt service is channeled, without increasing the budget deficit, then growth could accelerate by 0.5 point per year.

The reference 29 conducting an econometric analysis of panel data (68 countries, 1970-1991 period) also seem to validate the debt burden hypothesis for African countries in general: in the equations that explain the rate real growth per capita on the one hand, the investment rate on the other hand, the variable external debt ratio is significant, albeit slightly in the second case. According to their estimates, a reduction in the debt ratio (external debt divided by GNP) of 10% would lead to an increase in the growth rate of African economies of 0.3%, and a 0.4% increase in the rate of investment.

The reference 30 using a simultaneous equation estimation procedure, also highlighted a public debt effect on low-level private investment (elasticity of -0.03) but strongly significant. However, it is clear that their results show no effect of public debt on public investment.

The reference 22, in turn, empirically examined the disincentive effect and the crowding-out effect of the debt burden using panel data for a sample of fifty-three low- and middle-income countries during the 1990s. In their model, they used the investment-to-GDP ratio as a function of the growth rate, the debt-to-export service ratio, the illiteracy rate approximated by the level of capital underdevelopment and the lagged value of the investment rate. The results of their estimation show that the ratios of the debt-to-export ratio and the debt-to-income variable are significant at the 1% level. As for the debt service, it has a significantly negative coefficient. These results support the existence of a crowding out effect on private investment.

The reference 11, examining the experience of thirteen highly indebted countries from 1971 to 1992, finds a significantly negative relationship between the level of external debt and private investment at the 1% level. He also argued that the debt burden affects private investment through two channels:

Ÿ The first is that of the direct effect of disincentives which gives rise to fears of the appropriation of the funds invested by the State in order to service the debt;

Ÿ The second channel is the indirect effect that is manifested through adjustment measures undertaken to address debt servicing difficulties, such as import reductions and declining public sector investment.

The reference 31 produce the same results using panel data for a sample of fifty-three low- and middle-income countries during the period 1970-1999. UNECA (1998) examined the dynamic effects of external debt on the rate of private investment in Africa. The article shows how, in a country that exceeds the critical threshold of external debt accumulation, negative effects on private investment develop. The results of this study showed that most African countries could not reverse the trend during the period 1970-1994. He says the problem of external debt in Africa has led to the collapse of private investment. According to the findings of this same study, the debt burden begins to affect private investment from a critical threshold of 33.5% of debt accumulation relative to GDP. This study goes further by indicating that beyond the accumulated debt, the burden of its service makes the problem more complicated and thus it is difficult to stimulate investment and consequently growth.

The reference 32 in its empirical study of thirty-three countries in sub-Saharan Africa also finds arguments in favor of the hypothesis of the virtual burden of debt. While tests to assess the effect of the virtual debt burden have been conclusive for most panel data, the same is true for some studies applied to isolated countries.

The reference 33 also shows that the impact of indebtedness on private investment in a sample of Latin American countries is generally positive before 1981 (except in Mexico), but that it has fallen sharply after crisis of 1982, without becoming systematically negative. In addition, it shows that the sensitivity of private investment to other determinants is changing after the debt crisis.

Studies were also carried out for some particular African countries. For example, 13 assessed the impact of external debt on investment and growth in a study of Kenya during the period 1970-1999. His findings show that current debt flows stimulate growth and private investment while the flows of the old debt depress them. He also showed that the debt service ratio crowds out private investment at a statistically significant 12%. However, changes in the past debt service ratio positively affect the investment to a percentage of three points.

Many empirical studies have demonstrated the effect of public investment on private investment. The conclusions can differ as to the nature of this impact. Some authors have achieved complementarity, while others have confirmed the hypothesis of the crowding out effect. The idea of an eviction effect has long prevailed, especially in the elaboration of structural adjustment programs. On the other hand, endogenous growth models have tended to revive the role of public investment in increasing private investment.

In addition, there are few empirical arguments for developing countries on the issue, and several studies have confirmed that the effect depends on the degree of complementarity or substitutability between public investment and private investment. The reference 9 by examining the relationship between indebtedness and private wealth accumulation in 23 countries over the period 1975-1987, interpreted the relationship between public investment and private investment as long-term complementarity and short-term substitutability.

In a study conducted in September 2007 by the Department of Economic Studies and Currency of the BCEAO on the structure of public spending, private investment and economic growth in WAEMU. The assumption of positive externalities of public spending on growth was permissible and was tested in this study. More specifically, it was a question of analyzing, on the one hand, the nature of the link between public investment and private investment in UEMOA countries. On the other hand, it was necessary to analyze the impact of the composition of public spending on growth. The nature of the link between public investment and private investment in UEMOA countries was analyzed using a simple flexible accelerator model. The results obtained established the existence of a ripple effect of public investment on private investment in Côte d'Ivoire, Togo and to a lesser extent in Niger. However, the ripple effect could not be highlighted in Benin, Burkina Faso, Mali and Senegal. The composition of public spending has been decisive in the dynamics of growth in the union. Thus, the increase in the volume of public investment spending was just as beneficial to growth as the increase in its share of total government expenditure.

Ÿ Positive effect

Economists have become increasingly interested in the relationship between private investment and public investment. The reference 12 studies the possibility of a relationship of complementarity or substitutability between public investment and private investment in developing countries. Their study focused on the behavior of private investment in 24 developing countries. They drew on the investment accelerator model and came to the conclusion that the level of private investment was positively related to the change in real GDP anticipated and negatively influenced by the excess of the ability to invest. Another important result of their study was that the level of private investment was positively influenced by the trend in the level of public investment in infrastructure. In this regard, 34 estimated that the empirical result of 12 showed that "it is the public capital, long to implement, and therefore expensive in terms of installation, which acts positively on the private investment". Also 12 found a significantly positive coefficient for the infrastructure component of public investment.

The reference 34 shows in an empirical analysis of private investment that sought to establish the influential relationship between public investment and private investment for four low-income and four middle-income African countries during the 1970s and 1980 using error correction modeling and panel data modeling also find that public investment is positively correlated with private investment in both groups of countries with a strong complementarity impact in those with income way.

Other authors such as 12, 35 have also shown that the public investment rate globally has a positive influence on private investment in developing countries 13.

Although all these studies have confirmed the existence of a positive effect of public investment on private investment, there are many others that have had a negative effect.

Ÿ Negative effect

The reference 8 made a study on the impact of public debt on investment in Niger. The period studied was that from the year 1970 to the year 2000. Among the steps taken by the author to achieve the results was that of the examination of the importance of investment in an economy as well as the examination of the link between public investment and private investment. It resulted in the result that in the long term, public investment negatively and significantly influences the rate of private investment. When the state increases the public investment rate by 10%, the private investment rate decreases by 0.9%.

In addition, other work has been approached in this direction. This is the case of 13 who shows in his study of Kenya that public investment crowds out private investment, although its coefficient is not statistically significant. The reference 30 also obtain a slightly negative relationship between the stock of private capital and the stock of public capital.

Compared to all the above mentioned works, ours presents peculiarities in the sense that it wants to study the temporal aspects close to the current date by integrating in its analysis the last years that these other works had not taken into account. The importance of the sample in the fact that the PANEL data will even be the key to this work is also necessary, especially since we will have to deal with a huge sample. What other writers did not do except some reports from international organizations.

In addition, the insufficiency of such studies for the ECGLC countries, will make our work a particularity in the sense that it is interested in a whole economic region of enormous importance in terms of economic potential, human, hospital, Etc.

Analysts have so far relatively little studied the determinants of public investment in low-income developing 36. In 2001, Jan-Egbert Sturm of the University of Constance (Germany) modeled public investment in developing countries using three sets of determinants:

Ÿ Structural variables such as population growth;

Ÿ Economic variables such as real GDP growth, public debt, budget deficits and external assistance;

Ÿ Politico-institutional variables to measure, for example, political stability. Sturm found that the politico-institutional variables are less significant than the structural and economic variables. (We did not take this into account in our empirical analysis of public investment, not only because institutional variables proved to be inefficient in explaining public investment in developing countries, but also and especially because of the lack of concrete data).

In view of all the other models taken into account in the empirical lessons, we model public investment as a function of the state-guaranteed public external debt stock, the public debt service ratio and guaranteed by the government. State, the real GDP growth rate, public development aid, budget deficits and the population growth rate.

In 1989, 9 examined the relationship between indebtedness and private wealth accumulation in 23 countries over the period 1975-1987. The model they used links the private investment rate to the real GDP per capita in current dollars and its growth rate, the public investment rate, the inflation rate measured on the price index to the consumption, namely the service ratio [ratio between debt service (interest + amortization of the year) and exports of goods and services] and the debt ratio measured by the ratio between the debt stock and the GDP, these two ratios being offset by one period and a vector of the dummy variables to take account of possible shocks or disturbances affecting the rate of private investment. They considered three sub-periods (1975-1978, 1978-1982, 1982-1987) on which they regressed the model.

In view of all the other models taken into account in the empirical lessons, we model private investment as a function of public investment, the stock of public external debt and guaranteed by the State, the service ratio of the public and publicly guaranteed debt, interest rate, domestic credit, terms of trade, real exchange rate, inflation rate, and real GDP growth.

In the framework of data collection, analysis and data processing, the econometric tests are based on annual macroeconomic series expressed in $ and%, covering the period from 1960 to 2015 (55 years) and using the database of the World Bank (CD-ROM, World Bank Indicators, 2015), the IMF (International Monetary Fund) and the reports and annexes of the national banks of the ECGLC member states.

The specifications used to model public investment are based on the models proposed by 16 and taken up by 14 in their study entitled "Can Debt Relief Boost the Growth of Poor Countries?" ". Private investment is modeled on the simple flexible accelerator model with a specification borrowed largely from 9. Although the specifications of the authors mentioned above are different from ours in the choice of variables, there is a certain similarity as to the form chosen. However, it has been of paramount importance to introduce two notions relating to the public debt, namely: the stock of external public debt and guaranteed by the State as well as the ratio of the service of the public debt and guaranteed by the State.

Thus, to measure the impact of public debt on public investment as formulated in the first hypothesis, the public investment model adopted is written as follows:

| (1) |

In addition, an estimation will be made to highlight the impact of public investment on private investment and the impact of debt on investment, formulated alternately in the second and third hypotheses. Private investment in ECGLC countries is analyzed from a simple flexible accelerator model in which it is assumed that the production technology is characterized by a fixed relationship between the desired capital stock  and the expected level of production

and the expected level of production  The simplest form of the accelerator model is given by the equation:

The simplest form of the accelerator model is given by the equation:

| (2) |

The capital stock  adjusts according to the difference between this desired capital stock and the capital stock of the previous period.

adjusts according to the difference between this desired capital stock and the capital stock of the previous period.  at the speed β. So,

at the speed β. So,

| (3) |

Partly borrowing the Greene and Villanueva specification (1989) 9, the adjustment speed β is modeled by the following equation:

| (4) |

Private investment  is determined by the current capital stock and the capital depreciation rate

is determined by the current capital stock and the capital depreciation rate  according to the following relationship:

according to the following relationship:

| (5) |

With

Using the delay operator L defined by  for any X, the private investment is written:

for any X, the private investment is written:

| (6) |

Assuming that  that is, the capital depreciation rate remains equal to the capital stock adjustment speed, the long-term equation of private investment then write:

that is, the capital depreciation rate remains equal to the capital stock adjustment speed, the long-term equation of private investment then write:  In fact, in the long run,

In fact, in the long run,  and it can be postulated that

and it can be postulated that  for a given quantity

for a given quantity  Thus, the private investment equation (INVPR) is given by:

Thus, the private investment equation (INVPR) is given by:

| (7) |

Before proceeding with data analysis{6}, if the analysis procedure authorizes, it is necessary to carry out two preliminary tests to avoid any fallacious regression: stationarity test and that of cointegration. The stationarity of the series is justified if the mean and the variance are constant over time and if the value of the covariance between two periods does not depend on the time at which the covariance is calculated. Thus, the non-stationarity of a series manifests itself through two components: the presence of a deterministic trend and / or a stochastic tendency.

For model coefficients estimate, knowing that the equations are expressed in logarithm generated by the software in order to directly obtain the elasticities of certain variables (at least for the variables expressed in $ USD). By introducing from now on the long-term relation that will be the subject of the cointegration test, the specified models are written in the following way:

| (8) |

| (9) |

For panel model estimate, starting from the double dimension, individual and temporal that the model of Panel must contain, two tests are carried out: The first one which was of capital importance allows to specify the individual effects for our panel by seeking to discriminate the fixed and random effects. The second one is the homogeneity test and the Hausman specification test. So, it is a question of making a choice between the model of error components or model of random effects and the model of the effects of fixity. If we have to opt for the fixed effects model that are of the form:  our specified models will be written as follows :

our specified models will be written as follows :

| (10) |

| (11) |

The figures above describe the characteristics of the variables of interest for the three member countries of the Great Lakes economy. According to Jarque-Bera probability, we see that all variables of interest are affecting the absence of the normality hypothesis, their P-Value are less than 5% (0.05). However we can graphically summarize the same statistics for each of these countries (see Figure 2).

The four figures presented above sufficiently prove a certain homogeneity of the descriptive characteristics of the variables of interest.

5.2. Econometric Analyzes of DataIt is interesting to identify the effect associated with each country, that is, an effect that does not change over time, but varies from one country to another. This effect can be fixed or random. In addition to the question of individual effects, the questions of correlation and heteroskedasticity are examined in the context of the data in our possession as well as the question of selection bias, which will also be taken into account to complete certain tests.

According to individual effects presence test, we start by checking if there are indeed individual effects in our data. These effects can be represented by an intercepts peculiar to each country  We therefore try to test the null hypothesis

We therefore try to test the null hypothesis  in the regression

in the regression

|

| (12) |

which is a modeling of the individual effects.

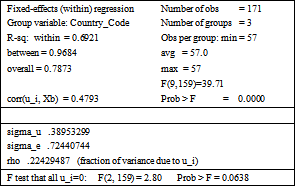

Since for the first model (INVPRI), the probability associated with the Fisher test is greater than 5%, we invalidate the null hypothesis that there is a common intercept for this model, which is different for the second model. Thus, individual effects must be included in the first model. To capture the individual effects related to the first model, we will use the "within" estimator (which is the same as the addition of dichotomous variables) which measures the variation of each observation relative to the average of the country to which it belongs observation

| (13) |

The individual effects are therefore eliminated and the MCO estimator can be used on the new variables of the first model.

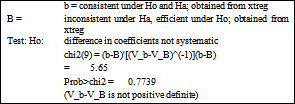

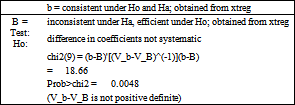

The Hausman test is a specification test that determine if coefficients of the two estimates (fixed and random) are statistically different. Under the null hypothesis of independence between the errors and the explanatory variables, the two estimators are unbiased, so the estimated coefficients should be slightly different.

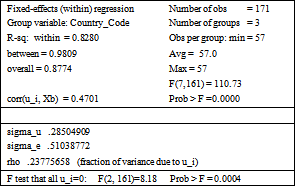

The results follow a χ2 law with K-1 degree of freedom. For the first model, the p-value (0.7739) being higher than the confidence level (5%), we reject the null hypothesis of the presence of the fixed effects, so for this model we will use the random effects that are effective if there is no correlation between errors and explanatory variables. On the other hand, for the second model, the p-value (0.0048) being higher than the confidence level (5%) we will use the fixed effects for this model.

The hypotheses of homoscedasticity and correlation must be verified. Four tests make it possible to verify if our data respect these hypotheses in the context. With regard to the hypothesis of homoscedasticity (test 1 and test 2), we must check if the variance of the errors of each individual is constant: for every individual i, we must have  for all t. For correlation, the new aspect to pay attention to is the possibility of correlation of errors between individuals (test 3). It must also be verified that the errors are not autocorrelated for each individual (test 4).

for all t. For correlation, the new aspect to pay attention to is the possibility of correlation of errors between individuals (test 3). It must also be verified that the errors are not autocorrelated for each individual (test 4).

To test the heteroscedasticity of the residues, we use the Breusch-Pagan Test considering the random effects for the first model and the fixed effects for the second model:

The null hypothesis in this case is that all the coefficients of the regression of the residues squared are zero, in short there is homoscedasticity. The alternative hypothesis is that there is heteroscedasticity. Thus, for both models, we reject the null hypothesis ("p-value" <alpha) of homoscedasticity, we can conclude to the presence of heteroscedasticity.

So we have  for all i, t which necessarily implies that

for all i, t which necessarily implies that  for all t and

for all t and  for everything i. It is not necessary to perform the test of inter-individual heteroscedasticity (Modified Wald test) which is considered here as test 2.

for everything i. It is not necessary to perform the test of inter-individual heteroscedasticity (Modified Wald test) which is considered here as test 2.

Since the second model does not contain individual effects and has fixed effects, the analysis is continued with the correlation test (test 3). However, for the first model although this is theoretically possible, some software like STATA does not allow to test the correlation if our model includes random effects (so we continue to test 4). As heteroscedasticity has been concluded in an attempt to obtain more information on the form of heteroscedasticity, GLS (GLS) is used for the second model where:

| (14) |

For the second model contemporary correlation between individuals, to test the correlation presence of inter-individual errors for the same period, therefore:  for

for  we use the Wald test. The null hypothesis of this test is the independence of residues between individuals. This test verifies that the sum of the squares of the correlation coefficients between the contemporary errors is approximately zero. Since it is only necessary to test those under the diagonal, the resulting statistic follows a law of 𝜒2 of degree of freedom

we use the Wald test. The null hypothesis of this test is the independence of residues between individuals. This test verifies that the sum of the squares of the correlation coefficients between the contemporary errors is approximately zero. Since it is only necessary to test those under the diagonal, the resulting statistic follows a law of 𝜒2 of degree of freedom  equivalent to the number of restrictions tested. After the test under STATA 12.0 on the corrected panel, the value obtained on the 𝜒2 associated with the Wald test which is 1256.14 with a p-value of 0.0000 which is lower than the critical value (0.05), we confirm the null hypothesis: the errors are not correlated in a contemporary way.

equivalent to the number of restrictions tested. After the test under STATA 12.0 on the corrected panel, the value obtained on the 𝜒2 associated with the Wald test which is 1256.14 with a p-value of 0.0000 which is lower than the critical value (0.05), we confirm the null hypothesis: the errors are not correlated in a contemporary way.

For the first model autocrorrelation intra-indivudal, we try to check if the errors are autocorrelated  for

for  of autoregressive form (AR1):

of autoregressive form (AR1):

| (15) |

We perform a Wald test whose null hypothesis posits no autocorrelation of errors. STATA 12.0 produced the following results, the 𝜒2 associated with the Wald test is 95.18 with a P-Value de 0.0000 which is less than the critical value (0.05), and so errors of the indivuduals are not autocorrelated.

For the first model (Private investment, INVPRI), we will begin by conducting preliminary tests applied to the time series (stationarity and cointegration) before making the estimates themselves.

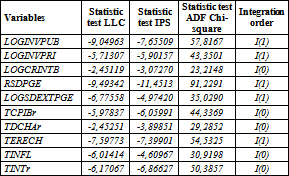

In order to detect the possible presence of unit root in our series and to the extent that our methodological framework takes possible existence of structural heterogeneities among nations in our sample, we implement second-generation unit root tests. Thus, we used the unit root tests of 37 (which imposes the same autoregressive coefficient for all series) and 38 (which allows a heterogeneity of the coefficients) with a special look at the ADF-Fisher test. So, for our series. The Table 7 summarizes the tests of Levin-Lin-Chu (LLC), the Im-Pesaran-Shin (IPS) test and the increased Dickey-Fuller test using the Chi-square test (ADF-Fisher Chi-square).

Unit root tests indicate that public investment under log, log private investment, the log of the public debt stock and guaranteed by the state, the ratio of public debt service and guaranteed by the state as well as that the terms of trade are assigned a unit root (see Table 7). The selection of lags numbers for each variable is calculated from Schwarz info criteron. Turning to the first differences, we find that all the aforementioned series become stationary.

We draw conclusions that they are integrated order one {I(1)} for the model with trend and constant that we used for these tests.

As public investment under log, private investment in logarithm, the logarithm of the stock of public debt and guaranteed by the state, the ratio of service of the public debt and guaranteed by the state as well as the terms of trade are integrated of order 1, there is a risk of cointegration.

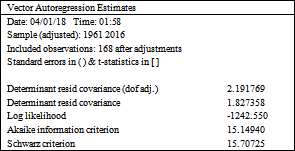

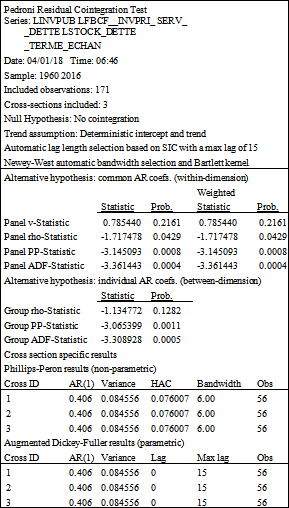

We apply cointegration techniques to test the presence of long-term relationships between integrated variables. With regard to this test, for the first step, we started by determining the number of lags (from the VAR model (p) applied to all stationary series with a first difference) before conducting the Pedroni cointegration test which is suitable for the cointegration of Panel series such as ours.

Table 8 tells us that the number of lags associated with the cointegration test, which is determined by the Akaike Information Criterion and Schwartz Criterion is 15, this number will be applied for the cointegration test. For the latter, we apply Pedroni tests that take into account heterogeneity through parameters that can vary between individuals.

Thus, for the second step, we test the null hypothesis of the absence of cointegration by the procedure developed by 39. This procedure, which aims to test cointegration in a Panel, consists of seven statistics that follow asymptotically the reduced normal centered law and that are based on a model that assumes that cointegration vectors are heterogeneous.

According to Table 9, five of the seven statistics invalidate the null hypothesis of no cointegration if we consider a level of significance equal to 5%. This leads us to conclude that there is a long-term relationship between our variables. The presence of a cointegration relationship is justified not only by three intra-dimensional type statistics called the parametric variance ration test (the rho-statistic panel, the pp-statistic panel and the ADF-statistic panel), but also by two other cross-dimensional statistics (The pp-statistic Group and ADF-statistic Group).

As a result, the set of tests related to cointegration analyzes shows the existence of a cointegration relationship. In the following lines, we will estimate the long-term relationship of cointegration using the most appropriate methods for this type of approach.

Since the selection of our variables and the periods considered were made on the basis of factors outside the study framework, this leads us to simplify the selection bias by using least squares as estimators.

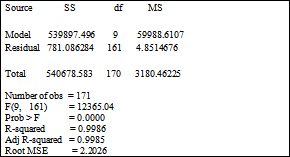

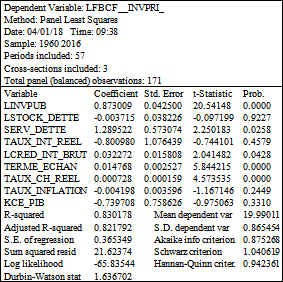

The explanatory powers of our model are high. On the whole in the short term for the countries of the economic community of the countries of the Great Lakes, public investment, the ratio of service of the public debt and guaranteed by the State, the gross domestic credit, the terms of trade as well real exchange rate positively impact private sector investment. On the other hand, the government-guaranteed stock of public debt, the real interest rate, the rate of inflation as well as GDP growth tend to crowd out private investments. So the estimated equation is as follows:

| (16) |

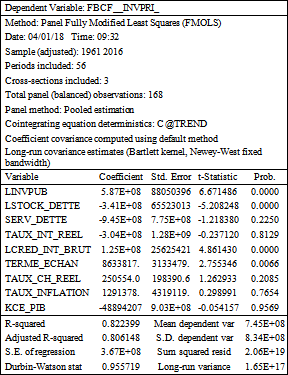

Given the existence of the long-term relationship between our variables (see Cointegration Test), we will estimate the long-term relationship of our variables by Folly-Modified Ordinary Least Square (FMOLS) methods.

In estimating long-term relationships, we maintain that for the member countries of the economic community of the Great Lakes countries, in the long term, public investment, gross domestic credit, trade terms, real exchange rate as well as the rate of inflation positively influence private investment. On the contrary, the government-backed and publicly guaranteed debt stock, the government-backed and publicly guaranteed debt service ratio, and GDP growth have a negative influence on private investment. Then, we pursue appling correction coefficient associated with recall force.

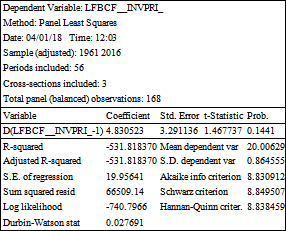

The correction coefficient associated with the restoring force is positive and not significant (4,830,523). There is therefore no mechanism for error correction: in the long term, the imbalances between the variables do not evolve in the same direction. This confirms the failure to take into account an error correction model for our case.

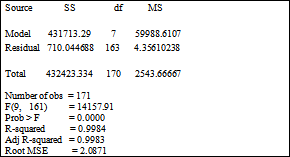

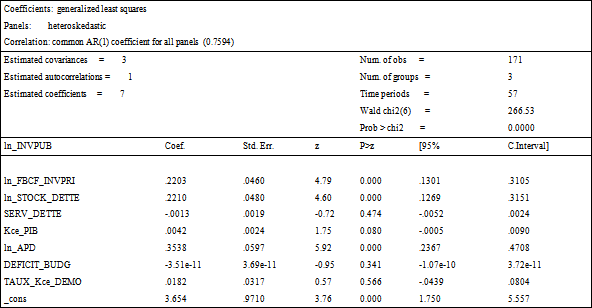

Regarding the second model, in order to obtain more information on the form of heteroscedasticity, we then use the Generalized Least Squares (GCM):

The table above estimates the public investment model. Thus, private investment, government-guaranteed stock of public debt, real GDP growth rate, official development assistance and population growth rate positively influence public investment differently than the service ratio public debt and guaranteed by the State and the budget deficit which negatively influences it.

The table above estimates the public investment model. Thus, private investment, government-guaranteed stock of public debt, real GDP growth rate, official development assistance and population growth rate positively influence public investment differently than the service ratio public debt and guaranteed by the State and the budget deficit which negatively influences it.

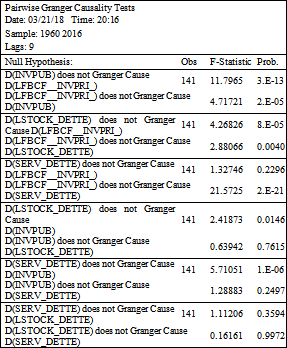

To conduct some tests such as the Granger causality test, we need to determine the number of p-model p (p) lags with the four first-difference stationary variables that are involved in this test and represent our series interest. For this purpose the criteria Akaike Info Criterion (AIC) and Schwarz Info Criterion (SIC) are used.

The table above tells us that there is a two-way causality between public investment and private investment, the same is true for the causal relationship between the stock of debt and private investment private investment causes debt service and not the opposite. The stock of debt and the service of the debt cause in the sense of granger the public investment and not the opposite.

In this section, it is a question of making an economic discussion of the results, of engaging the implications in terms of the economic policies, to make an overview on the future perspectives and to present at the end the different limits of this work.

6.1. Economic Discussion of Results and Verification of Research HypothesesOur analyzes show that the stock of public and publicly guaranteed debt has a negative impact on private investment both in the short term and in the long run, but this relationship is reversed when it comes to the relationship between the stock debt and public investment. We can therefore conclude that in cases of the presence of the negative effects of the existence of the heavy burden of debt reduces the incentive to invest for countries under-studies. Investors see the high burden of debt as a future tax on their income. The majority of these investors are a class of modern entrepreneurs who are able to appreciate the degree of indebtedness of the country, anticipate the consequences of the heavy burden of debt on their activities through future taxation given that the public power will always want to overtax in the future to be able to repay the debt and interest.

The high stock of debt also affected the credibility of ECGLC member states in terms of their ability to meet commitments. High debt leads creditors to no longer continue to lend to the States and this results in the decrease of financing contributing to the realization of the investments whose budgetary revenues can’t make it possible to realize them. This result was supported by several empirical conclusions previously developed, notably those of 11 and 13. These results test one of our initial hypotheses, which postulated that the high stock of public debt depresses investment (public and private).

On the other hand, the stock of debt tends to increase public investment in the member nations of the economic community of the Great Lakes countries, and this is due to the fact that by borrowing more, we do so in such a way as to finance ourselves so much investments in major public works, despite the return operations and other diversions that are taking place in the land-use planning sector in some of the ECGLC member countries.

However, the coefficient measuring the effect of the stock of debt on private investment is significant in some economies. This is certainly related to the restructuring of some ECGLC economies now dominated by formal, easily taxable activities. Investors in this area consider the effect of the debt burden in their investment decision.

Moreover, the negative influence of public debt service on investment (long-term relationship between private investment and debt service and the relationship between public investment and debt service) is due to In the long run, the government devotes the resources from customs revenue to the payment of external debt service rather than to investment expenditure and this has an impact in the long run on the level of investment of private actors.

The non-significance of the coefficient sign in the private investment model is due either to a volume effect of exports or to the fact that the debt has undergone several treatments ranging from rescheduling to cancellation. Even if it remains above the threshold considered tolerable, its evolution is decreasing.

Private investment has a positive impact on public investment and targets whether we are in the short or long term. As far as theoretical approaches are concerned, the explanation for this result can be found in the fact that the unprecedented increase in public investment made up of infrastructure-like infrastructure such as communication channels that link markets to one another to break the isolation of entire regions, to increase the opportunities for firms and to enable them to achieve significant economies of scale, which is to encourage private companies to settle in this promising environment. This result confirms our second hypothesis that public investment positively impacts private investment in ECGLC member states.

The various results thus found will allow us to make a number of recommendations in terms of economic policy such as the redefinition of policies in favor of debt cancellation, the development of public investment policies to promote the activities of the country, the private sector and the implementation of export promotion strategies and the attractiveness of foreign investors. These policies can reduce the public debt of ECGLC member countries to a tolerable level and thus encourage the revival of investment.

7.1. Pursuing Policies to Cancel Debt Policies to Reduce Public Debt should be UndertakenThe partners of the ECGLC member states have moreover recognized the over-indebtedness of these states because they consider it unsustainable. It is in this context that these States were admitted among the countries benefiting from the Heavily Indebted Poor Countries Initiative (HIPC). The governments of these countries must pursue economic and structural reforms, promote good economic and political governance in order to benefit more from these initiatives. The advantage of such an approach is to completely and definitively release the country from the burden of this debt which can not only dissuade public investments but also asphyxiate the emergence of private investments

7.2. Development of Public Investment Policies Favoring the Promotion of the Private SectorPublic investments will have to be targeted and targeted so that they can play their role of complementarity or support for private investment. This presupposes that state interventions must be directed towards investment spending with short and long-term effects such as education, health, public infrastructures (roads, railways, rural installations, hydraulic ...). The crucial role of public infrastructure has been recognized by NEPAD. In this sense, ECGLC member states should increase the volume of investment in infrastructure by reducing the risks that private investors face. Particular emphasis should be placed on the efficiency of these investments, particularly in public procurement and enforcement procedures, avoiding corrupt practices.

The State must also continue its policy of disengagement from the productive sector by completing the privatization program of public enterprises. This will enable him to avoid competing with the private sector, to which he must give the opportunity to play his full role. Government policies should then be limited to promoting a favorable business-friendly environment and creating stable macroeconomic and social conditions to minimize the external risks to economic operators. However, it must ensure that these privatizations are done in a transparent manner.

7.3. Strategies to Promote and Diversify ExportsIn this study we emphasized that we can’t separate the debt crisis of a country from the fall in prices of its main export product. This allowed us to make recommendations for the promotion and diversification of export products. For example, many of the models that have studied debt sustainability compare the interest rate with the growth rate of GDP or exports. Once this indicator is believed, we can conclude that the debt is at an intolerable level.

The states of the economic community of the Great Lakes countries must reduce their borrowing to increase the financing of public investment sources at a certain level of the increase in private investment and devote themselves to what these countries can present as resources even if indebtedness will be a heavy burden for future generations. That is, the ECGLC member countries still have to rely much more on the financial resources they receive internally through tax or other means to finance their investment programs. However, this tax must be balanced so as not to negatively influence private sector investment.

Like any research work, ours also suffers from a number of limitations. The first limit is related to the source diversity of the data relating to the same variable (World Bank, International Monetary Fund, different national banks of the States under-study). It would still be useful to determine the threshold beyond which the public debt of the ECGLC member states negatively affects the rate of public or private investment. This is a second limitation that future research focusing on the same theme could incorporate into their analysis. Finally, the fact that we have considered the Panel model as a whole conceals the realities of each ECGLC country, other researchers can conduct state-by-state analyzes. The limits thus underlined do not in any way diminish the relevance of the conclusions which we have reached and which confirm certain assertions developed in our review of the literature.

Our main objective in initiating this study was to examine the effects of public debt on public and private investment. This led us to first present all the different theoretical and empirical approaches to the issue and introductory approaches before making a brief presentation of the methodology. The individual effects tests were conducted and supported by the hausman specification test, after having tested the homogeneity and correlation of the errors of our models.

The individual effects tests concluded that these so-called individual effects were uniquely present for the private investment model, and that the random effects for the same model were different from the public investment model, which contains random effects in application of the hausman test. Thus, with the fixed effects associated with the heterogeneity of the data for the public investment model, we applied the Least Squares Generalized.

As for the private investment model, we went through all the steps before we went to the estimates by testing the stationarity using the LLC, IPS and ADF-Chi square methods and that led us to test the cointegration of some of our series. The result was that the series were wedged together and this led us to estimate long-term relationships of the private investment model with the use of Fully-modified OLS.

At the end of the estimates we noted that for ECGLC, public investment positively influences private investment and vice versa, hence the complementary and substitutability character. In addition, the stock of public and publicly guaranteed debt has a positive influence on public investment and at the same time has a negative influence on private investment. Finally, the negative influence between investment (private short-term and public) and debt service is reflected in our analyzes differently from the relationship between private short-term investment and debt service, which is a relationship positive. These estimates have generally confirmed our assumptions. The different implications and recommendations taking into account the results were given in point 4.

We do not pretend to have touched on all the aspects related to this theme, nevertheless the few pithy aspects give an important base. Other researchers can approach in the same direction as we by insisting on the study of the debt sustainability of ECGLC member states.

1. The 1982 crisis is not the first of its kind. For a history of debt crises, see Toussaint (2001), Millet and Toussaint (2002).

2. The "Eurodollars" refer to the dollars lent in the 1950s by the United States to the European Nations, notably through the Marshall Plan to finance their reconstruction. From the 1960s, European private banks are therefore full of capital, mainly made up of these "Eurodollars", and they will then seek to lend them so that they generate profits. As for "petrodollars", it is the dollars from oil. From 1973, the rise in the price of oil (the so-called "oil shock") brought comfortable incomes to the producing countries that placed them in the western banks. For them to benefit, these banks then granted loans on advantageous terms.

3. For Burundi, outstanding debt rose from 1.1% to 1.0% between 2014 and 2015. For the DRC, outstanding debt increased from 1.5% to 1.4% between 2015 And for Rwanda, the outstanding public debt rose from 0.7 to 0.6% between 2014 and 2015.

4. For Burundi, the public debt service ratio rose from 8.8 to 13.7% between 2014 and 2015. For the DRC, the ratio of public debt service rose from 3.1 to 3.3% between 2014 and 2015 and for Rwanda, the ratio of public debt service rose from 2.2 to 3.4% between 2014 and 2015.

5. For Burundi, the investment rate rose from 29 to 28% between 2014 and 2015. For the DRC, the investment rate rose from 22 to 21% between 2014 and 2015 And for Rwanda, the rate of investment rose from 26% to 25% between 2014 and 2015.

6. This study uses statistical and econometric tools to test assumptions made using EVIEWS version 8.0, STATA 12.0 and the Excel 2010 operator.

| [1] | MILLET, D., & TOUSSANIT, E. (2012). 65 questions, 65 réponses sur la dette. La FMO et la Banque mondiale. | ||

| In article | |||

| [2] | NAUTET, M., & MEENSEL, V. (2013). Impact économique de la dette publique. Bruxelles: De Boeck. | ||

| In article | |||

| [3] | BERR, E. (2005). La dette des pays en développement : bilan et perspectives. Université Montesquieu-Bordeau IV. | ||

| In article | |||

| [4] | IMF. (2010, Octobre). Perspectives de l’économie mondiale: Reprise, risques et rééquilibrage, Études économiques et financières. | ||

| In article | |||

| [5] | CARTON, B. (2013). Dette et croissance. Editions La Découverte. | ||

| In article | |||

| [6] | MBUYI, M. (2008). Droit international public, Cours inédit, G3 Droit,. UNIGOM. | ||

| In article | |||

| [7] | WARNER, A. (1992). Did the debt crisis cause the investment crisis? Quaterly Journal of Economics, 107 (4). | ||

| In article | View Article | ||

| [8] | GAIDAM, M. (s.d.). Impact de la dette publique sur l’investissement au Niger, Mémoire DEA. Université Cheikh Anta Diop, 106. | ||

| In article | |||

| [9] | GREEN, J., & VILLANUEVA, D. (1991). Private lnvestment in Deve1loping Countries. IMF Staff Papers. | ||

| In article | View Article | ||

| [10] | SERVEN, L., & SOLIMANO, A. (1993). Debt crisis, adjustment policies and capital formation in developing countries. World Development. | ||

| In article | View Article | ||

| [11] | DESPHANDE, A. (1997). The debt overhang and the disincentive to invest. Journal of development Economics, 52. | ||

| In article | View Article | ||

| [12] | BLEJER, M., & KHAN, M. (1984). Government policy and private investment in developing countries. IMF staff papers, 31 (2). | ||

| In article | View Article | ||

| [13] | WERE, M. (2001). The impact ofexternal debt on growth and private investment in Kenya: An empirical assessment. Working paper, Kenya Institute for public policy research and analysis. | ||

| In article | |||

| [14] | CLEMENTS, B., BHATTACHARYA, R., & NGUYEN, T. (2005). L’allégement de la dette peut-il doper la croissance des pauvres ? FMI. | ||

| In article | |||

| [15] | Bank World. (2015). Bilan de l’exercice. Washington D.C: Word Bank. | ||

| In article | |||

| [16] | J.-E. STURM (2011), Explaining IMF Lending Decisions after the Cold War, The Review of International Organizations, vol. 6. | ||

| In article | View Article | ||

| [17] | Eggertsson & KRUGMAN (2012), Debt, deleveraging, and the liquidity trap: A fisher-Minsky-Koo approach, Quarterly Journal of Economics. 127(3). | ||

| In article | View Article | ||

| [18] | TORNELL & VALESCO (1992). The tragedy of the commons and economic growth: Why does capital flow from poor to rich countries? Journal of Political Economy, 100(6): 1208-1231. | ||

| In article | View Article | ||

| [19] | COHEN, D. (1993, June). Low Investment and Large LOC Debt in the 1980's. American Economics Review. 436-449. | ||

| In article | |||

| [20] | Raffinot, M. (1998). Soutenabilité de la dette extérieure: de la théorie aux modèles d'évaluation pour les pays à faible revenu. Document de travail. | ||

| In article | |||

| [21] | FITZGERALD, A. H. (1992). Empirical investment equations for developing countries in striving. World Bank. | ||

| In article | |||

| [22] | ELBADAWI, I., NDULU, B., & NDUNGU, N. (1997). Debt overhang and economic growth in SubSaharan, in External finance for low-income countries. (Z. I. (eds.), Éd.) International Monetary Fund. | ||

| In article | |||

| [23] | HOFMAN, B., & REISEN, H. (1990). Debt Overhang, Liquidity Constraints and Adjustement Incentives. OECD Developpement Centre Working Paper (30). | ||

| In article | |||

| [24] | HANSEN, B. E. (2001). Econometrics of Structural Change: Dating Breaks in U.S. Labour Productivity. Journal of Economic Perspectives, 15 (4), 117-128. | ||

| In article | View Article | ||

| [25] | BURAK, G., & RAFFINOT, M. (2001). Surendettement et effet d'éviction: le cas de la Turquie. La Turquie et le Développement. | ||

| In article | |||

| [26] | Banque Mondiale (1989), L’Afrique Sub-saharienne, de la crise à une croissance durable, Etude de prospective à long terme, Washington D.C. | ||

| In article | |||

| [27] | CHOWDHURY, K. A. (1994). Structural Analysis of External Debt and Economic Growth: Sorne Evidence from Selected Countries in Asia and Pacific. Applied economics, 26. | ||

| In article | View Article | ||

| [28] | International Monetary Fund. (1990, Juin). Growth, External, and Sovereign Risk in Small Open Economy. (S. p. Fund), Éd.) Palgrave Macmillan Journals, 388-417. | ||

| In article | View Article | ||

| [29] | OJO, O., & OSHIKOYA, T. W. (1995). "Determinants of Long-Tenn Growth: Sorne African Results". Journal of African Economics , 4 (2), 163-191. | ||

| In article | View Article | ||

| [30] | DESSUS, S., & HERRERA, R. (1996, Mars). Capital public et croissance: une étude économétrique sur un panel des pays en développement dans les années 80. Mimeo, Centre de Développement. | ||

| In article | |||

| [31] | HJERTHOLM, P., LAURSEN, J., & WHITE, H. (1998). Macroeconomic issues in foreign aid. A paper presented at a conference of foreign aid, Development economics research group (DERG), Institute of economics, university of Conpenhagen. | ||

| In article | |||

| [32] | FOSUS, A. K. (1999). The External debt Burden and Economie Growth in the 1980s: Evidence from Sub-saharan Africa. Canadien Journal of Developmenl Studies. | ||

| In article | View Article | ||

| [33] | ROCKERBIE, D. (1994). Did the debt crisis cause the investment crisis? Further evidence. Applied Economies (26), 731-738. | ||

| In article | View Article | ||

| [34] | OSHIKOYA (1994), Macroeconomic Determinants of Domestic Private Investment in Africa: An empirical analysis, Economic Development and Cultural Change, vol 42, issue 3, 573-96. | ||

| In article | View Article | ||

| [35] | SUNDARARAJAN and THAKUR (1980), TUN WAI and WONG (1982), Fund-supported adjustment Programs and Economic growth, International Monetary Fund, Washington DC, (1985). | ||

| In article | |||

| [36] | International Monetary Fund, 2005. | ||

| In article | View Article | ||

| [37] | Levin, A. and Lin, C.F. (1992)/ Unit root n panel data; asymptotic and finite sample properties. Discussion Paper, No. 92-92; California, USA; University of California at San Diego. | ||

| In article | |||

| [38] | Im, K.S., Pesaran, M.H., Shin, Y. (1997). Testing for unit root in heterogenous panels. Mimeo. | ||

| In article | |||

| [39] | PEDRONI, P. (2001). Purchasing power parity tests in cointegration panels. Rev. Econ. Stat. 3 (A), 121 li. | ||

| In article | |||

Published with license by Science and Education Publishing, Copyright © 2019 Oliver Kasele, Lucien Momeka, Grace Bahaya and Bahati Ntumwa

![]() This work is licensed under a Creative Commons Attribution 4.0 International License. To view a copy of this license, visit

http://creativecommons.org/licenses/by/4.0/

This work is licensed under a Creative Commons Attribution 4.0 International License. To view a copy of this license, visit

http://creativecommons.org/licenses/by/4.0/

| [1] | MILLET, D., & TOUSSANIT, E. (2012). 65 questions, 65 réponses sur la dette. La FMO et la Banque mondiale. | ||

| In article | |||

| [2] | NAUTET, M., & MEENSEL, V. (2013). Impact économique de la dette publique. Bruxelles: De Boeck. | ||

| In article | |||

| [3] | BERR, E. (2005). La dette des pays en développement : bilan et perspectives. Université Montesquieu-Bordeau IV. | ||

| In article | |||

| [4] | IMF. (2010, Octobre). Perspectives de l’économie mondiale: Reprise, risques et rééquilibrage, Études économiques et financières. | ||

| In article | |||

| [5] | CARTON, B. (2013). Dette et croissance. Editions La Découverte. | ||

| In article | |||

| [6] | MBUYI, M. (2008). Droit international public, Cours inédit, G3 Droit,. UNIGOM. | ||

| In article | |||

| [7] | WARNER, A. (1992). Did the debt crisis cause the investment crisis? Quaterly Journal of Economics, 107 (4). | ||

| In article | View Article | ||

| [8] | GAIDAM, M. (s.d.). Impact de la dette publique sur l’investissement au Niger, Mémoire DEA. Université Cheikh Anta Diop, 106. | ||

| In article | |||

| [9] | GREEN, J., & VILLANUEVA, D. (1991). Private lnvestment in Deve1loping Countries. IMF Staff Papers. | ||

| In article | View Article | ||

| [10] | SERVEN, L., & SOLIMANO, A. (1993). Debt crisis, adjustment policies and capital formation in developing countries. World Development. | ||

| In article | View Article | ||

| [11] | DESPHANDE, A. (1997). The debt overhang and the disincentive to invest. Journal of development Economics, 52. | ||

| In article | View Article | ||

| [12] | BLEJER, M., & KHAN, M. (1984). Government policy and private investment in developing countries. IMF staff papers, 31 (2). | ||

| In article | View Article | ||

| [13] | WERE, M. (2001). The impact ofexternal debt on growth and private investment in Kenya: An empirical assessment. Working paper, Kenya Institute for public policy research and analysis. | ||

| In article | |||

| [14] | CLEMENTS, B., BHATTACHARYA, R., & NGUYEN, T. (2005). L’allégement de la dette peut-il doper la croissance des pauvres ? FMI. | ||

| In article | |||

| [15] | Bank World. (2015). Bilan de l’exercice. Washington D.C: Word Bank. | ||

| In article | |||

| [16] | J.-E. STURM (2011), Explaining IMF Lending Decisions after the Cold War, The Review of International Organizations, vol. 6. | ||

| In article | View Article | ||

| [17] | Eggertsson & KRUGMAN (2012), Debt, deleveraging, and the liquidity trap: A fisher-Minsky-Koo approach, Quarterly Journal of Economics. 127(3). | ||

| In article | View Article | ||

| [18] | TORNELL & VALESCO (1992). The tragedy of the commons and economic growth: Why does capital flow from poor to rich countries? Journal of Political Economy, 100(6): 1208-1231. | ||

| In article | View Article | ||

| [19] | COHEN, D. (1993, June). Low Investment and Large LOC Debt in the 1980's. American Economics Review. 436-449. | ||

| In article | |||

| [20] | Raffinot, M. (1998). Soutenabilité de la dette extérieure: de la théorie aux modèles d'évaluation pour les pays à faible revenu. Document de travail. | ||

| In article | |||

| [21] | FITZGERALD, A. H. (1992). Empirical investment equations for developing countries in striving. World Bank. | ||

| In article | |||

| [22] | ELBADAWI, I., NDULU, B., & NDUNGU, N. (1997). Debt overhang and economic growth in SubSaharan, in External finance for low-income countries. (Z. I. (eds.), Éd.) International Monetary Fund. | ||

| In article | |||

| [23] | HOFMAN, B., & REISEN, H. (1990). Debt Overhang, Liquidity Constraints and Adjustement Incentives. OECD Developpement Centre Working Paper (30). | ||

| In article | |||

| [24] | HANSEN, B. E. (2001). Econometrics of Structural Change: Dating Breaks in U.S. Labour Productivity. Journal of Economic Perspectives, 15 (4), 117-128. | ||

| In article | View Article | ||

| [25] | BURAK, G., & RAFFINOT, M. (2001). Surendettement et effet d'éviction: le cas de la Turquie. La Turquie et le Développement. | ||

| In article | |||

| [26] | Banque Mondiale (1989), L’Afrique Sub-saharienne, de la crise à une croissance durable, Etude de prospective à long terme, Washington D.C. | ||

| In article | |||

| [27] | CHOWDHURY, K. A. (1994). Structural Analysis of External Debt and Economic Growth: Sorne Evidence from Selected Countries in Asia and Pacific. Applied economics, 26. | ||

| In article | View Article | ||

| [28] | International Monetary Fund. (1990, Juin). Growth, External, and Sovereign Risk in Small Open Economy. (S. p. Fund), Éd.) Palgrave Macmillan Journals, 388-417. | ||

| In article | View Article | ||

| [29] | OJO, O., & OSHIKOYA, T. W. (1995). "Determinants of Long-Tenn Growth: Sorne African Results". Journal of African Economics , 4 (2), 163-191. | ||

| In article | View Article | ||