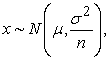

The forecast is very complex in financial markets. The reasons for this are fluctuation of financial data, Such as Stock index and rate interest data over time. The determining a model for forecasting fluctuations, can play a significant role in investor's decision making in financial markets. In the present paper, the Vasicek model the prediction of the rate interest on year later value, on using month data from the USA rate interest year 2017 and 2018, we will discuss, for this job, the first unknown parameters Vasicek model, as Average interest rate, Standard deviation of interest rate, and recursive mean of the model, using Euler maruyama maximum like lihood method, will be calibrate, and their values will be obtain by programming in the Maple software. And using a numerical method Euler Maruyama and computer simulation with the Maple software, for simulated data, gained averages and Standard deviations, confidence interval and their normal histogram will be the plot. Also, average of the solutions obtained from computer simulations is compared with real ones, and after analyzing and reviewing the results, performance of the Vasicek model will be measured, in interest rate value prediction. And in the end, this research is compared with internal article, and suggestions for future research will be raised.

The time structure of the rate interest is known as the rate of return on the curve, which measures the relationship between risk free rate and risk free ratios different outcomes. The study of this section relates to the rate of economic profit. The time structure emphasizes market prediction of future events by providing a complete table of interest rate over time. However a description of the time structure of the interest rate gives us a way to understand the exact information. We can use this information to predict how to changes the base variables for impact on the yield curve, to apply. The interest rate and its dynamics give a hard computational area in modern financial theory. The fixed income in the modern market does not only include debt securities and derivative types, but also depends on the rate of interest. The rate of interest is important in the valuations of all markets, in the decision-making of companies for investment, which is based on the rate of return, as well as the cost of capital, depends on the rate of interest. The rate of interest is influenced by the price of the market. How Mach money will be in the next year, or in the next year. In other words the time value of money is fully determined by interest.

1.2. Classical Models (Short Term Interest Rate)In the short-term interest rate model, which is based on dimensial space, we consider the momentum rate process. The risk-free rate of short-term interest is one of the most fundamental and crucial factors in determining financial markets. Most of these models are com only developed by scholars and researches in a continuous time structure, which provides a special farm work for short-term and risk-free rates. A series of interest rate models including the Merton model, the question we are looking for in this article is to answer it. Whether or not the performance a Vasicek model is suitable for valuing and predicting the value of the interest rate. The present article is presented in five sections, thus after the introduction in the first part, the second introduces the studies carried out in this field. In the third section, we present general introduction to the classical model of asset valuation, such as the Vasicek model, and basic concepts including random process, Stochastic differential equations, confidence interval, calibrations, and the method used in this study, namely, the Euler maruyama numerical method, and the mathematical equations are expressed. In the fourth part of the computer programing, the USA interest rate data will be express by Maple software. In the fifth section, performance of the vasicek model in the valuations interest rate will be evaluate, for in this job average of the answers obtained from the computer simulation compared on the real answers.

The subject we present in this article is a new and applicable subject. Similar work in this area found in the article by Steven Dumber in 2013 from the Department of mathematics at university of Nebraska-Link on obtaining the confidence interval for European put option has been highlighted by the Monte Carlo method 8. Finding the confidence interval for the options price by Monte Carlo simulation is a method using a random sample of a special distribution that produces a numerical solution for a mathematical model. The Monte Carlo method is a Statistical technique among various mathematical method that establishes a connection between a mathematical model and the rate of interest. By moving Brownian as a random model for the price process, we can use the Monte Carlo process to simulate the price option. We assume that the price is modeled as a geometric Brownian motion, so we can get its normal distribution function at the time of expiration. N the pseudo random number  from the normal distribution of the stock price models, then we approximate the price of the sales option with the expected yield:

from the normal distribution of the stock price models, then we approximate the price of the sales option with the expected yield:  the average sample:

the average sample:

| (1) |

Which  is a normal distribution with mean:

is a normal distribution with mean:  and Variance

and Variance  is, as a result, normal distribution:

is, as a result, normal distribution:

| (2) |

This expression states the value  estimated by the Monte Carlo simulation method has the expected yield:

estimated by the Monte Carlo simulation method has the expected yield:  which is the standard deviation by

which is the standard deviation by  divisibility. Most carefully we remember the normal distribution of the standard

divisibility. Most carefully we remember the normal distribution of the standard  then by the normal distribution properties, we can build an confidence interval with a confidence level of 0 .095 which is as follow:

then by the normal distribution properties, we can build an confidence interval with a confidence level of 0 .095 which is as follow:

| (3) |

William Harley of department of mathematics and computer at the royal military university of Canada in 2011 has been working under an accidental strike to obtain a confidence interval for discounted equity cash dividends. 3 in this paper, the method for discounting stock profits is a com on method in most financial books, generally, the Gordon growth model is one of the techniques used to calculate the cost of equity capital. Gordon assumes that the trend of dividend yield increases daily with constant geometric growth rates, and it assumed that the stock return on profits will follow a steady path in the future. The purpose of this paper is to build a confidence interval for discounted cash benefits under random variables. Also in the thirteen year of john halls book in 2013, the Black Scholes model has been valued and two-way confidence interval obtained for this model. 4, 5 but our goal here is determination confidence interval for the interest rate by the Vasicek model. Also published newly jobs in year 2019, can mentioned to Discretizing the Information Based Asset Price Dynamics on Black Scholes, BHM, and Heston on Euler scheme and Milstein scheme.

The type of our research in this paper is applied, the method used in the study of Euler-Maruyama numerical method, the data used, the USA interest rate in 2017 and 2018, and in the analysis of data from the Maple software used. In the following, we gave general over view of the variables studied in this paper, such as the Vasicek model, the stochastic differential equation, the random process, the Euler Maruyama numerical, and the confidence interval and calibration, and gives definition of them.

3.1. Vasicek ModelThe Vasicek model introduced in 1977 by Vasicek 10. In financial, vasicek is a short-term interest rate model that can use market risk. This model can also use in valuation of the interest rate of the derivative instrument. Also this model is consistent with the market index, which can applied when the market index is disturbing. This model can be seen as a random investment process, which applies to the stochastic differential equation below:

| (4) |

Which  is a wiener process. Attributes:

is a wiener process. Attributes:

1. The parameter a is the average return rate of the model relative to the parameter b used to adjust the rate of interest change.

2. The parameter b is the average return on interest.

3. And σ the Random fluctuations measured in the model.

As the relationship  increased when it a decreases, it increases

increased when it a decreases, it increases  the speed of the system, and the stability depends

the speed of the system, and the stability depends  on the average b over the period. Vasicek model is one of the first models to calculate the average recurrence rate of the system, which is one of the main characteristics of financial pricing, and, if the level is too high, disrupts economic activity, and reduces the rate of interest. The parameter

on the average b over the period. Vasicek model is one of the first models to calculate the average recurrence rate of the system, which is one of the main characteristics of financial pricing, and, if the level is too high, disrupts economic activity, and reduces the rate of interest. The parameter  always tend to return to the average value. The factor

always tend to return to the average value. The factor  represent the momentary changes in interest at time t. if the parameter

represent the momentary changes in interest at time t. if the parameter  is set, the interest rate is fixed, i.e.

is set, the interest rate is fixed, i.e.  The value variable

The value variable  in the model must always be positive, so that stability created in the model. For example when, the rate of interest goes up, the parameter

in the model must always be positive, so that stability created in the model. For example when, the rate of interest goes up, the parameter  has the duty to bring it back to equilibrium. One the criticism of the Vasicek model is that the rate of interest may negatively affected by this model, which addressed in the CIR model.

has the duty to bring it back to equilibrium. One the criticism of the Vasicek model is that the rate of interest may negatively affected by this model, which addressed in the CIR model.

The Stochastic differential equation in which one or more variable are random process. In this modeling, white noise is usually used as a completely randomized parameter 1. This equation is generally written in the following form:

| (5) |

is called a standard Brownian motion (wiener process) 6, 7. Which has the following properties:

is called a standard Brownian motion (wiener process) 6, 7. Which has the following properties:

1. The beginning of the process is zero that is:

2. for each,  as

as  random variable

random variable  has a normal distribution with mean zero and variance

has a normal distribution with mean zero and variance

3. Has a Gaussian property, that is, for any  random variables

random variables  have a normal distribution.

have a normal distribution.

4. There are independent development.

5. Random variables  for

for  are independent.

are independent.

6. All sample paths B with a probability are continuous, but are now here decisive.

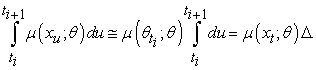

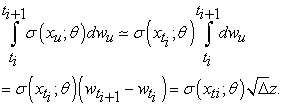

3.4. Euler Maruyama Numerical MethodThis numerical method used for computer programming in the next section of the Maple software, hence forth, in this section, we describe be feature of this method the Euler Murayama discretization method. This of the methods used for the discretization of the results. The method is equivalent to approximating integrals using the left end point rule when is  at time

at time  Hence integral approximated with respect:

Hence integral approximated with respect:

|

To the integral product of the time  and the integral rate

and the integral rate  2. means:

2. means:

| (6) |

The second part of the integral approximated as follows:

| (7) |

The Z random variable is standard normal 9, hence the discretization obtained as follows:

| (8) |

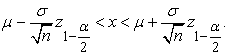

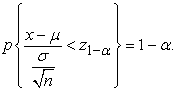

The Confidence interval is divided into two-way confidence intervals. The normal distribution range is as follows:  so if we

so if we  define, Z normal will be standardized. Therefore:

define, Z normal will be standardized. Therefore:  will be. So the two way confidence interval

will be. So the two way confidence interval  for the known variance state is a follows:

for the known variance state is a follows:

| (9) |

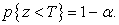

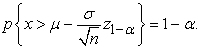

Also, the one-way confidence interval is dividend in two groups of on-sided left and right sides from the right, sometimes it's important for us x be more or less than a certain number, or if the image is less than a certain amount, then one-way confidence interval we use, as a result:

| (10) |

as a result:

as a result:  | (11) |

So the one-way confidence interval  from the right is:

from the right is:

| (12) |

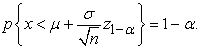

And one-way confidence interval on the left are the following:

| (13) |

Differential method used to estimate the parameter of random process that are modeling on using continues random time differential equations. Which includes estimating the maximum-magnitude parameter, which includes the maximum precision like lihood, approximate approximation maximization, partial conditionalization approach, and (MLE) estimation Euler-Murayama maximization, and hermitation polynomials. Based on the estimation function of the EF including the estimation function of the martingale and the torque method. For example, in estimating the maximum exact like lihood it assumed that distribution of the observed phenomenon considered only for the finite number of unknown parameters estimated by checking and selecting the values the maximize probability of sample values. Let's explain in the estimation method for Euler-Maruyama maximization.

In this section, we describe, the discretization of the Vasicek model with the Euler-Maruyama method, and then, using the USA interest rate data in 2017, 2018 and implementing with the Maple software, will evaluate the performance of the Vasicek model in valuation the rate of interest. We doing this job with the average of the solutions obtained on the computer simulations and compare it with real answers.

4.1. Implementation of the Vasicek ModelConsider the following Vasicek model:

| (14) |

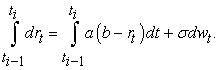

The discretization of the Vasicek model with the maximum likelihood of Euler Murayama in the interval  is as follows:

is as follows:

| (15) |

Therefore, with respect to the numerical integral approximation, we have:

| (16) |

The  random number is normal, therefore we have:

random number is normal, therefore we have:

| (17) |

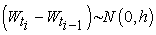

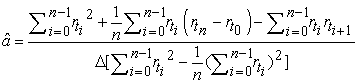

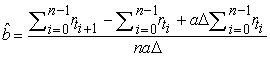

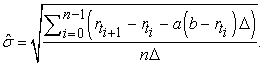

In the previous section, we have done the discretization of the model using the Euler Maruyama discretization method. In the long run, we want to implement Vasicek model based on the USA interest rate data in 2017, 2018 to do this, we must first to estimate the known parameters of the Vasicek model:

| (18) |

I.e.  recurrence mean, b mean, and

recurrence mean, b mean, and  standard deviation. Using Euler-Maruyama a like Lihood method, the known parameters of the Vasicek model obtained as follows:

standard deviation. Using Euler-Maruyama a like Lihood method, the known parameters of the Vasicek model obtained as follows:

| (19) |

| (20) |

| (21) |

In this section, we implement the Vasicek model with the USA interest rate data. We will get this data first from ''http://fred.stlouisfed.org/series/DEF/download data,'' which will monthly data for 2017:

We now calculate the known parameters of the Vasicek model based on the USA interest rate data, the first we rewrite the data of the interest rate Table 1 as follows:

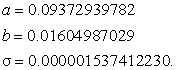

Therefore, on given the USA interest rate data in Table 2, and with the programming in the Maple software, the following numbers obtained for the known parameters of the model:

|

Therefore, with the parameters obtained above and the initial interest rate  we perform the simulation for the vasicek model based on the parameters obtained and the USA interest rate data in Table 2. Using the Euler Maruyama discretization and programming in the Maple software, we can plot the histogram for

we perform the simulation for the vasicek model based on the parameters obtained and the USA interest rate data in Table 2. Using the Euler Maruyama discretization and programming in the Maple software, we can plot the histogram for  data as follows: (number simulations of the program: 1000)

data as follows: (number simulations of the program: 1000)

Then, we find the average return, standard deviation, and Confidence interval for the data, which is as follows:

|

|

|

As in the next section, we do the same for data for 2018. We will get this data first from ''http://fred.stlouisfed.org/series/DEF/download data,'' which will monthly data for 2018:

We now calculate the known parameters of the Vasicek model based on the USA interest rate data in Table 3, the first we rewrite the data of the interest rate in Table 3 as follows:

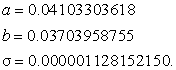

Therefore, given the USA interest rate data in Table 4, and with the programming in the Maple software, the following numbers obtained for the known parameters of the model:

|

Therefore, with the parameters obtained above and the initial interest rate  we perform simulation for the vasicek model based on the parameters obtained and the USA interest rate data in Table 4. Using the Euler Maruyama discretization and on programming in the Maple software, we can plot the histogram for

we perform simulation for the vasicek model based on the parameters obtained and the USA interest rate data in Table 4. Using the Euler Maruyama discretization and on programming in the Maple software, we can plot the histogram for  data as follows: (number simulations of the program: 1000).

data as follows: (number simulations of the program: 1000).

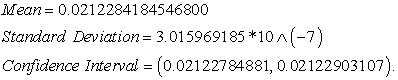

Then, we find the average return, standard deviation, and Confidence interval for the data for the obtained data, which is as follows:

|

As given that the value of  that is, the amount of interest rate in a year later, the amount USA interest rate in Table 2 for 2017 year is 0.0130, also the average of the answers obtained with computer simulation is approximately 0.01248, and the amount of interest rate a year later, in Table 4 for 2018 year is 0.0220, also the average of the answers obtained with computer simulation is approximately 0.02122, then answers given with computer simulation, to the real answers is near.

that is, the amount of interest rate in a year later, the amount USA interest rate in Table 2 for 2017 year is 0.0130, also the average of the answers obtained with computer simulation is approximately 0.01248, and the amount of interest rate a year later, in Table 4 for 2018 year is 0.0220, also the average of the answers obtained with computer simulation is approximately 0.02122, then answers given with computer simulation, to the real answers is near.

In the previous section, we implemented Vasicek model based on the USA interest rate data in 2017, 2018 on the Maple software, which yielded the following results, for 2017 year:

Ÿ Initial value of interest rate: 0.0065

Ÿ Value of one year later interest rate: 0.0130

Ÿ The average of the computer simulations obtained for the vasicek model: 0.0124

These results were also achieved for 2018 year:

Ÿ Initial value of interest rate: 0.0130

Ÿ Value of one year later interest rate: 0.0220

Ÿ The average of the computer simulations obtained for the vasicek model: 0.02122.

The results, show that the difference between the real and the computer simulation answers is very low and in a thousandth, and these results also show performance of the vasicek model in the valuation of the rate of interest.

5.2. Model ConstraintsThese model are suitable for short time periods, and because of the use of white noise without memory. These models improved using wiener Frazier.

| [1] | Bjork, T. (2009). Arbitrage theory in continuous time. Oxford university pres. | ||

| In article | |||

| [2] | Cyganowski, S., Kloeden, P., & Ombach, J. (2001). From elementary probability to stochastic differential equations with MAPLE. Springer Science & Business Media. | ||

| In article | View Article PubMed | ||

| [3] | Gordon, M. J. (1962). The investment, financing, and valuation of the corporation. RD Irwin. | ||

| In article | |||

| [4] | Hull, J. C., & Basu, S. (2016). Options, futures, and other derivatives. Pearson Education India. | ||

| In article | |||

| [5] | Hull, J., Treepongkaruna, S., Colwell, D., Heaney, R., & Pitt, D. (2013). Fundamentals. Of futures and options markets. Pearson Higher Education AU | ||

| In article | |||

| [6] | Klebaner, F. C. (2012). Introduction to stochastic calculus with applications. World Scientific Publishing Company. | ||

| In article | View Article | ||

| [7] | Øksendal, B. (2003). Stochastic differential equations. In Stochastic differential equations (pp. 65-84). Springer, Berlin, Heidelberg. | ||

| In article | View Article | ||

| [8] | Owen, A. B. (2013). Monte Carlo theory, methods and examples. Monte Carlo Theory, Methods and Examples. Art Owen. | ||

| In article | |||

| [9] | Rust, J. (1996). Numerical dynamic programming in economics. Handbook of computational economics, 1, 619-729. | ||

| In article | View Article | ||

| [10] | Seydel, R., & Seydel, R. (2006). Tools for computational finance. (Vol. 3). Berlin: Springer. | ||

| In article | |||

| [11] | Vasicek, O. (1977). An equilibrium characterization of the term structure. Journal of financial economics, 5(2), 177-188. | ||

| In article | View Article | ||

Published with license by Science and Education Publishing, Copyright © 2019 Mohammad Ali Jafari, Mehran Paziresh and Majid Feshari

![]() This work is licensed under a Creative Commons Attribution 4.0 International License. To view a copy of this license, visit

http://creativecommons.org/licenses/by/4.0/

This work is licensed under a Creative Commons Attribution 4.0 International License. To view a copy of this license, visit

http://creativecommons.org/licenses/by/4.0/

| [1] | Bjork, T. (2009). Arbitrage theory in continuous time. Oxford university pres. | ||

| In article | |||

| [2] | Cyganowski, S., Kloeden, P., & Ombach, J. (2001). From elementary probability to stochastic differential equations with MAPLE. Springer Science & Business Media. | ||

| In article | View Article PubMed | ||

| [3] | Gordon, M. J. (1962). The investment, financing, and valuation of the corporation. RD Irwin. | ||

| In article | |||

| [4] | Hull, J. C., & Basu, S. (2016). Options, futures, and other derivatives. Pearson Education India. | ||

| In article | |||

| [5] | Hull, J., Treepongkaruna, S., Colwell, D., Heaney, R., & Pitt, D. (2013). Fundamentals. Of futures and options markets. Pearson Higher Education AU | ||

| In article | |||

| [6] | Klebaner, F. C. (2012). Introduction to stochastic calculus with applications. World Scientific Publishing Company. | ||

| In article | View Article | ||

| [7] | Øksendal, B. (2003). Stochastic differential equations. In Stochastic differential equations (pp. 65-84). Springer, Berlin, Heidelberg. | ||

| In article | View Article | ||

| [8] | Owen, A. B. (2013). Monte Carlo theory, methods and examples. Monte Carlo Theory, Methods and Examples. Art Owen. | ||

| In article | |||

| [9] | Rust, J. (1996). Numerical dynamic programming in economics. Handbook of computational economics, 1, 619-729. | ||

| In article | View Article | ||

| [10] | Seydel, R., & Seydel, R. (2006). Tools for computational finance. (Vol. 3). Berlin: Springer. | ||

| In article | |||

| [11] | Vasicek, O. (1977). An equilibrium characterization of the term structure. Journal of financial economics, 5(2), 177-188. | ||

| In article | View Article | ||

){kind=link}

){kind=link}

{kind=link}

{kind=link}

){kind=link}

){kind=link}

{kind=link}

{kind=link}