High internal control is the cornerstone of an enterprise’s development. It is worth noticing that as Small and Medium Enterprises (SMEs) have received attention along their development, their internal control weakness has had a significant impact on enterprises’ credit. Starting from SMEs’ current state of internal control, this paper selects SMEs in manufacturing industry from 2017 to 2020 as a sample, draws forth weakness and their influences that existed in internal control among which difficulty in credit stands out as a major problem, and finally looks into direct effect of internal control on an enterprise’s credit. In the research, the degree of lack of internal control is determined as the independent variable, and status of credit is determined as the dependent variable. The paper has measured the data set with standard indicators, and has filtered and analyzed data. As the result the paper draws the conclusion that the quality of internal control is strongly related to credit in SMEs, and the low quality inflicts a series of problems, that is, investors of SMEs are hesitant to lend due to the imbalance of information and lack of trust from banks; consequently, SMEs suffer a setback due to this lack of lending. The more serious the internal control problem is, the more financial burdens SMEs have to bear. At the same time, an enterprise can ease the financial difficult by rectification but cannot completely solve the problem.

In an enterprise, internal control can be identified as an automatic alarming and maintenance system. Internal control assures high quality of accounting information, thus improving an enterprise’s awareness of risks, and protects assets of an enterprises, thus standardizing all management and operation activities. Especially for China, SMEs are major actors in the country’s economic play, and their achievements and contributions are not indispensable. Internal control as the adhesive that combines and merges all economic factors. After this merging process, internal control maximizes the combined forces of all these factors, thus profiting the enterprises. Therefore, a successful internal control helps with not only avoiding disadvantages in management decision but also providing decision makers important information, leading them to beneficial direction, and offering the best economic solution. Nonetheless, because of China’s economy background and characteristics of SMEs, internal control of SMEs is concerning and problematic, which severely affects an enterprise’s sustainable development. Without setting standards for internal control, SMEs can only formulate management system based on their own features and economic ability, which results in thoughtlessly copying other enterprises’ regulation or complete abandonment of internal control management. These weaknesses in internal control are presented in two ways. Internally speaking, unordered managerial and operational status leads to frenzy danger in financing risks. Externally speaking, once investors and banks detect disadvantages in SMEs, including low level of management and insufficient or distorted financial information, they are unwilling to loan or risk investing because of uncertainty in future profit. Thus, investigation in influence of low level of internal control on credit is especially valuable to current economic environment.

A benign internal control regulation highly benefits an enterprise, while a malignant regulation strikes down an enterprise. Difficulty in loaning is always a major obstacle to development of SMEs, and the problem brings many scholars and business owners to study and research in the area. Operation status is not optimistic due to the strong correlation between internal control weakness and loaning. Quite a few researchers have analyzed the cause of difficulty in loaning, which demonstrates the significance of the problem. Once again, insights about the correlation between internal control weakness and loaning difficulty is particularly valuable. This paper is dedicated to experimentally testing influence of internal control weakness based on theoretical analysis, therefore pushing SMEs to rethink their future development path.

One of major features of SMEs is imbalance of information, and it brings out severe adverse selection and moral risks problems. Therefore, loaning constraint is rather important. When banks decide whether they should lend or not, they normally turn down the case because it is difficult to gain the information about enterprises. In other words, transparency of information barely exists in SMEs; as the result, when a bank makes the decision about loaning to a SME, the bank needs to spend extra time and capitals to investigate the SME. It makes sense that a bank is not willing to engage in such a time-consuming and low-payback activity, and, therefore, we should not be surprised by the fact that banks are not willing to loan to SMEs in general, so the quality of internal control is determinant in terms of loaning success.

First of all, quality internal control positively guarantees accuracy and accountability of accounting information of an enterprise, alleviating imbalance of information between the bank and the enterprise. Though each SME is different from one another, but they are same in terms of miscellaneous process of management and daily operation. These SMEs need abundant accounting information to decide the next strategy, and accurate and factual financing information is the most important element for an enterprise to profit. Thus, a comprehensive and complete internal control regulation can lead a SME to beneficial path. In context of an accurate and undistorted accounting information, effective internal control provides a substantial foundation for validity and reliability of financial report, which reflects positive information to external stakeholders and potential investors, thus attracts more future investors. Besides, more accurate the information provides by SMEs is, more conveniently for a bank to attain and access SMEs, and more easily SMEs are able to gain loans from the bank.

Second of all, quality internal control is effective in terms of improving administrating level and extenuating agency problems. Credibility of business owners, styles of management, rational distribution of power and authorization are all decisive factors of an enterprise’s environment of internal control. A consummate environment determines performance of an enterprise under risks, suppresses self-beneficial behaviors of managers, and establishes regulations among employees. Setting up scientific and rational assessment system and precise and clear punishment and reward and promotion mechanism can effectively define each department’s responsibility, reinforce employees concept of duty, alleviate agency problem, and inspire management’s comprehensive vision of sustainable development. As the result, quality internal control is helpful in terms of developing efficient operation structure and sustaining shareholders’ benefit. Also, quality internal control decreases chance of opportunism in an enterprise, avoiding minor group with power manipulates the whole company. Therefore, benign internal control boosts probability that a bank loans to an enterprise after consideration and ensures consolidation of relationship between enterprises and banks.

Last but not least, quality internal control increases efficiency and magnifies effects of management. A comprehensive internal control regulation not only decreases chances of frauds by effective supervision but also assures carry out of legal institution. As a core system of management, internal control can be used as a weapon to wipe out risks from a business by strengthening originally weak parts of management. With further prompt conduction of information directing and balancing each major decision, a business owner can streamline the communication within the company and discover or prevent severe mistakes in time. Furthermore, a comprehensive internal control creates a positive moral atmosphere and establishes a reputation and credibility for a company. With heightened reputation and credibility, the company can have less intense relationship with banks if it pays back principle and interest in time, and banks have no reason to reject request of loaning as a result.

On the other hand, if a SME does not have a fine internal control, banks will realize they have high risk loaning, thus rejecting loaning or offering tiny amount of loans in order to avoid risks, and the SME will suffer from loan constraint. Based on this logic, this paper formulates the hypothesis:

H: Internal control weakness is positively related to financing cost in SMEs, that is, the more internal control weakness, the more constraints on loaning.

This paper selects SMEs in manufacturing as research sample. Data about internal control and financing report are from Guotaian database and are all through strict screening.

3.2. Model SettingIn order to test hypothesis, we establish a function shown below.

|

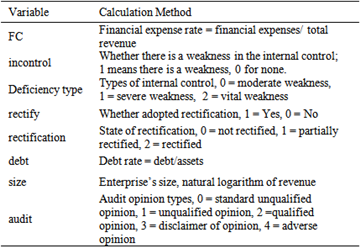

The dependent variable in this paper is financing cost, which reflects loaning problem of a SME. This paper also adopts financial expanse rate, which is financial expenses as a percentage of revenue, as a financial indicator.

The independent variable is internal control weakness, which is measured by whether a company has the weakness in internal control. Quality of internal control is studied through SMEs’ self report of internal control information and evaluations of registered public accountant, and these data are applied as evidences for hypothesis and data analysis. Moreover, in order to detect severity of internal control weakness, corresponding solutions, and further influence on loaning, this paper also introduces types of internal control weakness, appearance of rectification, and effects of rectification as another independent variables to further analyze financial expense rate.

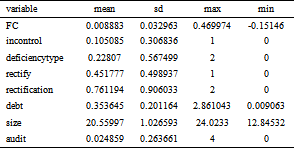

Variables presents in this paper are shown in table below. In order to lowering the risk of loaning, banks normally run a comprehensive assessment of an enterprise’s credibility and solvency, which reflects whether the business is able to pay the debt in time, before the bank loans. Also, we only select SMEs from manufacturing industry in this paper so that difference in characteristics is minimized. Beyond type of industries, size of business, another factor influencing loaning status, is also controlled.

|

This paper first runs descriptive statistics for all variables. From Table 1, mean value of financial expense rate is 0.8%, with minimum -15% and maximum 46%. This information tells us that SMEs significantly vary from each other in terms of financial expense caused by loaning, which reflects a great difference in loaning interest rate. SMEs need in-depth information about banks’ loaning conditions and act correspondingly, especially resolve internal control weakness, so that SMEs can decrease the difficulty of loaning. Meaning value of whether internal control weakness exists is 0.105, with minimum 0 and maximum 1. This information reflects flaw in internal control actually influences loaning difficulty of a SME. Mean value of audit opinion is 0.0248, with minimum 0 and maximum 4, which demonstrates that registered public accountants provide standard unqualified opinions in most cases, and only offer other opinions in a few cases.

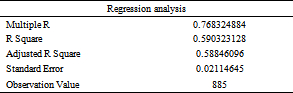

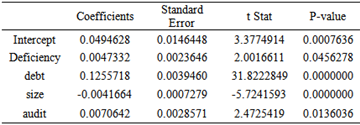

4.2. Research in Influence of Internal Control on LoaningIn this research, internal control is evaluated by whether the weakness exists in internal control. As shown in Table 2, coefficient of financial expense rate is positive, which illustrates that occurrence of internal control weakness necessarily increases financial cost and tightens loan constraint, proving the hypothesis of this paper. Therefore, establishment of internal control regulation ensures a business’s sustainable development. Once internal control is not regulated, a business faces many problems including weakness in management environment, illegal actions, inefficiency or failure of risk assessment mechanism, malpractice and mistakes caused by ineffective execution, failure of immediate feedback caused by poor conduction of information and communication, which all lead to financial adversity for a company. Moreover, reputation and credibility of the business will be at stake, and financial institutions will gradually lose confidence in the business and refuse to loan. On the other hand, even though banks are willing to loan to the SME, the business has high risk of not paying back the loan due to lack of reliable internal control regulation, and both banks and business will suffer from losing capitals. In general, banks will reject loaning once a SME has problem with its internal control regulation.

Beside coefficient of financial expense rate, coefficient of debt is also positive, reflecting that higher ability to pay the loan indicates higher ability to cope with disturbances and risks from market which pulls a business out of mire of financial adversity. Coefficient of size is negative, which shows bigger size leads to more serious financial difficulties. This correlation coincides with reality. Coefficient of audit is positive, demonstrating once a public registered accountant offers opinions that are not standard unqualified opinions, banks will not trust the SME, thus more likely rejecting loaning money to it.

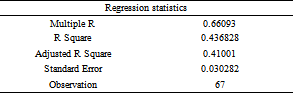

Through analysis of regression line, goodness of fit (R2) is high.

|

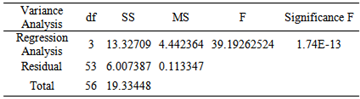

Through variance analysis, value of significance F reflects a clear correlation between internal control weakness and credit of loaning.

|

Finally, through regression analysis, P-value is smaller than significance level, reflecting a linear correlation between internal control weakness and credit of loaning.

4.3. Analysis of Flaw in Internal Control and RectificationThis part of research specifically inspects influence of severity of internal control weakness and change in internal control on loan credit.

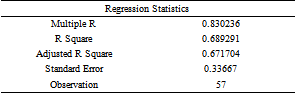

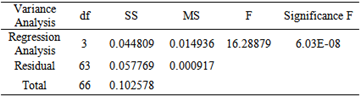

In Table 3, types of internal control weakness is set as independent variable, and we run a regression analysis of financial expense rate. Conclusion from the analysis is that loan constraint over SMEs are aggravated as internal control weakness increases. The cause of this phenomenon is that in a severe internal control weakness environment, lack of supervision and management leads to loss of confidence of banks in SMEs, which choose to reject loaning because it is risky lending money to a company that may not be able to repay its debt.

Through analysis of regression line, goodness of fit (R2) is high.

|

Through variance analysis, value of significance F reflects a clear correlation between types of internal control weakness and credit of loaning.

|

Finally, through regression analysis, P-value is smaller than significance level, reflecting a linear correlation between severity of in internal control weakness and credit of loaning: the more severe the weaknesses are, the higher the financial cost is.

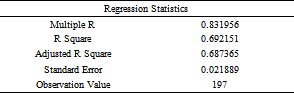

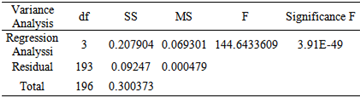

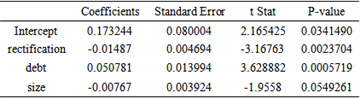

As demonstrated by Table 4 (whether a business adopted rectification as independent variable) and Table 5 (states of rectification as independent variable), rectification can alleviate financial constraint. Notice that this negative influence cannot be completely eradicated.

Through analysis of regression line, goodness of fit (R2) is high.

|

Through variance analysis, value of significance F reflects a clear correlation between whether a rectification is adopted and credit of loaning.

|

Finally, through regression analysis, P-value is smaller than significance level, reflecting a linear correlation between whether a rectification is adopted and credit of loaning.

Through analysis of regression line, goodness of fit (R2) is high.

|

Through variance analysis, value of significance F reflects a clear correlation between states of rectification and credit of loaning.

|

Finally, through regression analysis, P-value is smaller than significance level, reflecting a linear correlation between states of rectification and credit of loaning: more effective the rectification is, lower the financial cost is.

The research selected a group of SMEs in manufacturing from 2017-2020 as sample from 2017-2020 and inspected relationship between internal control defect and loaning credit. The general conclusion is that in internal control weakness creates huge financing difficulty and loan intense constraint. The more severe the weaknesses are, the more difficult the loaning is for SMEs, and the more rigorous the whole financial environment for SMEs is. If SMEs immediately adopt corresponding solutions and rectification, they can improve from their loaning adversity and reduce negative effect of internal control weakness; though they may not completely eradiate this negative influence, rectification is beneficial in terms of future loaning activities. Therefore, quality of internal control has inseparable relationship with loaning in SMEs and affects a SME’s ability to raise funds in the future, so it is emergent to pay attention to internal control regulation.

The research looks into linkage between internal control weakness and loaning of SMEs and provides solid evidences for the influence of this linkage. Since SMEs in manufacturing are studied as the sample for this research, this paper also suggests several strategies that A SME can take to maintain a healthy growth:

1. From SME’s stand point, they should improve their quality of internal control. A good example is the best sermon, so SMEs should start overhauling their internal control system if there is any, reflecting on their own weakness, establishing a sound foundation for internal control, and focusing on solving the internal control problem. As internal regulation becomes gradually comprehensive and consummate, SMEs will achieve a smooth finance circulation.

2. From environmental perspective, government and businesses should work together to establish a rational and authoritative evaluation organization over internal controls in SMEs. SMEs along cannot solve their loaning difficulty without a trustworthy financial environment. A effective evaluation organization can function as a bridge between SMEs and financial institutions, providing information to both SMEs and financial institutions: SMEs can learn from feedback given by the evaluation organization and thus improve based the feedbacks; financial institutes can effectively attain the financial information they need to decide whether to loan or not. With supports from the policy, government can create a trustworthy external financial environment for SMEs.

| [1] | Zhonghua Liu,Hongyu Liang. The Credit Restraint Effect of Internal Control Defects. Auditing and Economic Research, 2015(2): 13-20. | ||

| In article | |||

| [2] | Li Xing. On the Internal Control of Small and Medium sized Enterprises and the Prevention of Bank Credit Risk. Financial Accounting, 2009(3): 73-77. | ||

| In article | |||

| [3] | Jiang Zhao, Zongxian Feng. An Empirical Analysis of the Constraints on Credit Financing of SMEs. Finance and Finance, 2007(5): 45-46. | ||

| In article | |||

| [4] | Zhai Sun. The problems and countermeasures of internal control in small and medium-sized enterprises. China's collective economy, 2015(10): 49-50. | ||

| In article | |||

| [5] | Zanjun Ma. An Analysis of the Credit Financing of Small and Medium sized Enterprises in China, 2008(7): 58-60. | ||

| In article | |||

| [6] | Xuzhao Xiao. Strengthen the research on credit business risk management of small and medium-sized enterprises. North China Finance, 2006(10): 24-28. | ||

| In article | |||

| [7] | Hui Chen. An Analysis of the Reasons and Countermeasures for the Difficulty in Credit of Small and Medium sized Enterprises in China, 2007(12): 185-186. | ||

| In article | |||

| [8] | Hongxin Fang, Yunyun Jin. Corporate Characteristics, External Audit and Voluntary Disclosure of Internal Control Information -- Empirical Research Based on 2003-2005 Annual Reports of Shanghai Listed Companies [J]. Accounting Research, 2009(10): 44-52. | ||

| In article | |||

| [9] | Juqin Shen,Shifeng Yan. A Study on the Market Response to the Disclosure of Internal Control Self evaluation Report -- Based on the Data of Listed Companies on Small and Medium Board in 2010 [J]. Nanjing Audit Institute, 2013 (1): | ||

| In article | |||

| [10] | Doyle J, Ge W, McVay S. Determinants of weakness in internal control over financial reporting[J]. Journal of Accounting and Economics, 2007, 44(1): 193-223. | ||

| In article | View Article | ||

| [11] | Doyle J, Ge W, McVay S. Accruals quality and internal control over financial reporting.[J].The Accounting Review, 2007, 82(5): 1141-1170. | ||

| In article | View Article | ||

| [12] | Wanfu Li, Bin Lin, Lu Song. The Role of Internal Control in Corporate Investment: Efficiency Promotion or Inhibition? [J]. Managing the world, 2011(2): 81-99. | ||

| In article | |||

| [13] | Weian Li, Wentao Dai. The Relationship Framework of Corporate Governance, Internal Control and Risk Management -- Based on the Strategic Management Perspective [J]. Audit and Economic Research, 2013(4): 3-12. | ||

| In article | |||

Published with license by Science and Education Publishing, Copyright © 2022 Xiaoyi Zhang

![]() This work is licensed under a Creative Commons Attribution 4.0 International License. To view a copy of this license, visit

http://creativecommons.org/licenses/by/4.0/

This work is licensed under a Creative Commons Attribution 4.0 International License. To view a copy of this license, visit

http://creativecommons.org/licenses/by/4.0/

| [1] | Zhonghua Liu,Hongyu Liang. The Credit Restraint Effect of Internal Control Defects. Auditing and Economic Research, 2015(2): 13-20. | ||

| In article | |||

| [2] | Li Xing. On the Internal Control of Small and Medium sized Enterprises and the Prevention of Bank Credit Risk. Financial Accounting, 2009(3): 73-77. | ||

| In article | |||

| [3] | Jiang Zhao, Zongxian Feng. An Empirical Analysis of the Constraints on Credit Financing of SMEs. Finance and Finance, 2007(5): 45-46. | ||

| In article | |||

| [4] | Zhai Sun. The problems and countermeasures of internal control in small and medium-sized enterprises. China's collective economy, 2015(10): 49-50. | ||

| In article | |||

| [5] | Zanjun Ma. An Analysis of the Credit Financing of Small and Medium sized Enterprises in China, 2008(7): 58-60. | ||

| In article | |||

| [6] | Xuzhao Xiao. Strengthen the research on credit business risk management of small and medium-sized enterprises. North China Finance, 2006(10): 24-28. | ||

| In article | |||

| [7] | Hui Chen. An Analysis of the Reasons and Countermeasures for the Difficulty in Credit of Small and Medium sized Enterprises in China, 2007(12): 185-186. | ||

| In article | |||

| [8] | Hongxin Fang, Yunyun Jin. Corporate Characteristics, External Audit and Voluntary Disclosure of Internal Control Information -- Empirical Research Based on 2003-2005 Annual Reports of Shanghai Listed Companies [J]. Accounting Research, 2009(10): 44-52. | ||

| In article | |||

| [9] | Juqin Shen,Shifeng Yan. A Study on the Market Response to the Disclosure of Internal Control Self evaluation Report -- Based on the Data of Listed Companies on Small and Medium Board in 2010 [J]. Nanjing Audit Institute, 2013 (1): | ||

| In article | |||

| [10] | Doyle J, Ge W, McVay S. Determinants of weakness in internal control over financial reporting[J]. Journal of Accounting and Economics, 2007, 44(1): 193-223. | ||

| In article | View Article | ||

| [11] | Doyle J, Ge W, McVay S. Accruals quality and internal control over financial reporting.[J].The Accounting Review, 2007, 82(5): 1141-1170. | ||

| In article | View Article | ||

| [12] | Wanfu Li, Bin Lin, Lu Song. The Role of Internal Control in Corporate Investment: Efficiency Promotion or Inhibition? [J]. Managing the world, 2011(2): 81-99. | ||

| In article | |||

| [13] | Weian Li, Wentao Dai. The Relationship Framework of Corporate Governance, Internal Control and Risk Management -- Based on the Strategic Management Perspective [J]. Audit and Economic Research, 2013(4): 3-12. | ||

| In article | |||