sciepub.com

sciepub.com

Quick Submission

Quick Submission

Effects of Credit on Agricultural Inputs and Technology in the Nkoranza North District, Ghana

Eric Kwadwo Appiah1, Richard Baah-Mintah2, , Ellen Owusu-Adjei2

, Ellen Owusu-Adjei2

1Eguafo-Abrem Senior High School, Komenda-Edina-Egufo-Abrem Municipality, Ghana

2Anglican University College of Technology, Nkoranza Campus- Ghana

Abstract

The study sought to address the question as to whether agricultural credit affects maize productivity in the Nkoranza North District (NND). The study employed the quasi-experimental and a cross-sectional survey design using the ‘with and without’ method in assessing the effects of microcredit on the production levels of small scale farmers in the district. In all, a total of 310 respondents were randomly selected for the study. Respondents were then grouped into farmers with and without credit. Questionnaire was used to collect data from the respondents. Graphs and tables were used to present descriptive aspect of the results while the independent sample t-test was used to examine the effect of credit on inputs and agricultural technology. The study revealed that credit largely and positively influences the acquisition of agricultural inputs such as fertilizers, pesticides and herbicides, as well as hiring of labour and acquisition of more farm lands and technology. The study concludes that microcredit improves maize production in the NND. It is recommended that farmers must join the farmers’ associations in their communities to facilitate their access to credit and must use their loans for the intended purposes.

Keywords: credit, agricultural input, technology, Ghana

Copyright © 2016 Science and Education Publishing. All Rights Reserved.Cite this article:

- Eric Kwadwo Appiah, Richard Baah-Mintah, Ellen Owusu-Adjei. Effects of Credit on Agricultural Inputs and Technology in the Nkoranza North District, Ghana. American Journal of Rural Development. Vol. 4, No. 6, 2016, pp 134-142. http://pubs.sciepub.com/ajrd/4/6/3

- Appiah, Eric Kwadwo, Richard Baah-Mintah, and Ellen Owusu-Adjei. "Effects of Credit on Agricultural Inputs and Technology in the Nkoranza North District, Ghana." American Journal of Rural Development 4.6 (2016): 134-142.

- Appiah, E. K. , Baah-Mintah, R. , & Owusu-Adjei, E. (2016). Effects of Credit on Agricultural Inputs and Technology in the Nkoranza North District, Ghana. American Journal of Rural Development, 4(6), 134-142.

- Appiah, Eric Kwadwo, Richard Baah-Mintah, and Ellen Owusu-Adjei. "Effects of Credit on Agricultural Inputs and Technology in the Nkoranza North District, Ghana." American Journal of Rural Development 4, no. 6 (2016): 134-142.

| Import into BibTeX | Import into EndNote | Import into RefMan | Import into RefWorks |

At a glance: Figures

1. Introduction

Microcredit has emerged as one of the effective ways of helping the poor to help themselves especially in the developing world. A World Bank study has shown evidences of wide ranging impacts of microcredit [1]. Arguing from sociological perspective, Otero [2] indicated that access to credit provides the poor with productive capital that helps to build up their sense of dignity, autonomy, and self-confidence, and hence are motivated to become participants in the rural economy. In growing economies, microcredit is capable of transmitting benefits of growth to the citizenry through the informal sector. It is well documented that lack of microcredit is a critical constraint to the establishment or expansion of viable agricultural enterprises. Microcredit, therefore, assists small scale farmers to purchase inputs needed to increase output levels [3].

The Nobel peace winner, Professor Muhammad Yunus intimated that microcredit is based on the premise that the poor have skills which remain unutilized or underutilised. It is definitely not the lack of skills which make poor people poorer. He added that charity is not the answer to poverty. It only helps poverty to continue. It creates dependency and takes away the individual’s initiative to break through the walls of poverty. He therefore proposed that unleashing the energy and creativity in each human being is the answer to poverty. According to [25] two-thirds of the world population does not have access to financial services. He further argues that credit will break the vicious cycle of poverty as money begets money [25].

The World Bank, the United Nations agencies and other world leaders have over the years been committed to the growth of agriculture in order to ensure food security in the world. The 2008 World Bank Report stressed the commitment of the Bank to continue with its rural policies and has clearly pointed out that agriculture is the key to poverty alleviation especially for African smallholder farmers. It has made various allocations towards agriculture since its establishment. The World Bank and other agencies in 2009 and 2010 distributed about three billion dollars to developing nations [4, 5].

Agricultural credit seems to have worked well in many countries and notable among them is India. India has systematically pursued a supply led approach to increase agricultural credit. Its objectives have been to replace moneylenders to relief farmers of indebtedness, and to achieve high level of agricultural credit, investment, and output. India’s success in this direction has been described as outstanding [6] and Syria has also performed well with credit [7].

According to the impact chain model developed by Hulme, all microfinance programmes operate on the assumption that intervention will change human behaviours and practices in ways that lead to desired outcomes [8]. [9], indicate that in order to increase agricultural production, there is the need to enhance the level of technological innovations. This also calls for the strengthening of the financial capacity and a major determinant in this respect, is credit. Rahji (as cited in [9] has observed that credit is a basic tool of production which provides farmers with capital to acquire resources in time, in the advantageous amount and in efficient manner. One of the major constraints for small-scale farmers to adopt agricultural technologies is credit [10].

Since Ghana’s Independence in 1957, several governments have made various attempts to promote rural development in an effort to improve the living standards of the rural people [11]. This has been done through improved agriculture. Agriculture is the main economic activity in Ghana. For instance, 92 percent of people living in the savannah zone are involved in agriculture. Out of the 3.4 million households involved in food crop production, 2.5 million cultivate maize. Cocoa and maize are the most important cash crops and the two most important crops grown in the forest zone of Ghana [12].

According to the Ghana living standard survey, out of 3.4 million households, 1.8 million hire labour on their farms while 1.9 million purchase locally made hand tools. In addition, more than 500,000 households spend on seeds, insecticide, herbicides and many others. The survey reported that out of the total GH¢ 352.6 million spent on all the different types of agricultural inputs, 89 percent is spent on crop inputs. Among the expenditure items, 43 percent is spent on hiring labourers and 19 percent on inorganic fertilizers.

In Ghana, the agricultural sector employs 55.8 percent of the population. In 2010, agriculture contributed 29.8 percent to Ghana’s gross domestic product (GDP) and 25.6 percent in 2011 [12]. There have been attempts by various governments since Ghana’s independence to make credits available particularly to rural dwellers whose major occupation is agriculture. These attempts have been the institution of policies and programme in order to achieve the objectives. Some of these policies and programmes include:

1. Establishment of banks to address the financial needs of the fisheries and agricultural sectors.

2. Establishment of the Rural Community Banks (RCBs) and the introduction of regulations such as commercial banks being required to set aside 20 percent of total portfolio, to promote lending to agriculture and small scale industries in the 1970s and early 1980s;

3. Shifting from a restrictive financial sector regime to a liberalised regime in 1986.

4. Promulgation of PNDC law 328 in 1991 to allow the establishment of different categories of non-bank financial institutions, including savings and loans companies, and credit unions [13].

These policies have brought about three categories of microfinance institutions. These are:

1. Formal suppliers such as Savings and Loans Companies, Rural and Community Banks;

2. Semi-formal suppliers such as Credit Unions, Financial Non-Governmental Organisation (FNGOs), and Co-operatives; and

3. Informal suppliers such as Susu collectors and clubs, Rotating and Accumulating Savings and Credit Association (RASCAs), traders, moneylenders and other individuals [13].

The efforts by successive governments in Ghana to promote agriculture have been exhibited in the establishment of banks as indicated earlier. Such banks established include the Bank of Gold Coast, now Ghana Commercial Bank, the National Investment Bank (NIB), and the Agricultural Development Bank (ADB). All these Banks were established purposely to provide financial assistance to rural people including small scale farmers.

However, as time went by it was evident that these banks were not able to shoulder the financial needs of the rural people. As a result, the government of Ghana through the Bank of Ghana (BoG) established the first Rural Bank on 5th July, 1976 at Agona Nyakrom in the Central Region [14, 15, 16]. Since then, there has been an increase in the number of rural banks in Ghana from one in 1976 to 136 fully operational banks as at 2012 [17]. Since their establishment, the rural banks have increased the capital base of most farmers especially small scale farmers.

According to the [18] out of the cultivable land of 8,808,600 hectors which is about 57 percent of Ghana’s total land area; only 24 percent is under cultivation. The [19] maintains that agriculture in Ghana is predominantly on a small holder basis, although there are large farms and plantations. For instance, about 60 percent of the average farm size is less than 1.2 hectares, 25 percent are between 1.2 and 2.0 hectares with only 15 percent above 2.0 hectares [20]. According to [21] small scale farms are classified to range between 0.1 hectare and 6.0 hectares.

Nkoranza North District is one of the rural districts in Ghana, in terms of development and this goes to confirm the assertion that most food crop producers in Ghana live in the rural areas - among the 63 percent of Ghanaians living in rural and semi-rural areas, agriculture employs 60 percent [22]. People in this district have also benefited from credit facilities including Micro-finance and Small Loans Centre (MASLOC) funds, and District Assembly’s assistance to farmers and traders, which are direct government sanctioned credit to the people. There is a rural bank, savings and loans institutions and other micro-finance institutions which grant credit to the people. Also present are Non-Governmental Organisations such as Adventist Development and Relief Agency (ADRA) who are lending helping hands to farmers in the District through credit.

Increased agricultural productivity is the wish and aspiration of governments especially in less developed nations where a larger percentage of the population is employed in the agricultural sector of which Ghana is no exception [13]. Nkoranza North District (NND) is one of the food baskets of the country. The major crops produced by the farmers are maize and yam. However, majority of them farm on small-holder bases, employ family labour in most cases, work on small pieces of land and use crude methods and implements in their farming activities. These undoubtedly affect their productivity and income. In order to improve upon these some of these farmers seek credit facilities from various sources available in the district. However, upon casual observation, it appears the hopes and aspirations of farmers with which they embarked on the credit business have not materialised. This therefore calls for a scientific enquiry to find out the extent to which credit is affecting the output of farmers.

In subsequent sections of this paper, the discussions will focus on conceptual issues of microcredit and small scale maize production, the methodology, and the empirical evidence on the effect of microcredit on small scale maize production in the Nkoranza North District. The last section of the paper features the conclusions and policy implications.

2. Microcredit and Small Scale Maize Production

Most definitions of credit seem to hover around giving assistance (cash/kind) to people who need them and the recipients paying later. For instance, [23] defines credit as “a temporary transfer of capital resource from an individual or institution to another person or institution for a specific period of time, purpose and at an agreed interest charge”. The Grameen Bank also defined microcredit programme as extending small loans to very poor people for self-employment projects that generate income, allowing them to care for themselves and their families. Also, it is the extension of small loans to entrepreneurs too poor to qualify for traditional bank loans (Grameen Bank, n.d). [24] seemed to agree with the microcredit summit and defined microcredit as a small capital given to the poor to do business.

The Nobel peace winner, Professor Muhammad Yunus intimated that microcredit is based on the premise that the poor have skills which remain unutilized or underutilised. It is definitely not the lack of skills which make poor people poorer. He added that charity is not the answer to poverty. It only helps poverty to continue. It creates dependency and takes away the individual’s initiative to break through the walls of poverty. He therefore proposed that unleashing the energy and creativity in each human being is the answer to poverty [25].

Agriculture constitutes a large share of national output and employs a majority of the labour force in most developing countries. It has been argued that given the size of the agricultural sector in most developing countries, its growth has implication not only for growth in other sectors but also for poverty and inequalities. This is partly due to the fact that agriculture is the largest employer in developing countries either directly or indirectly engaging more than half of the labour force [26, 27]. In order for agriculture to help in the development of rural areas, there are a lot of factors that need to be considered. Among such determinants is credit [3].

Agricultural credit has a lot of roles to play in the growth and development of the sector in most economies especially in less developed countries. For instance, [28] observed that increased productivity of farm resources comes from innovations that originate in the farm supply sector. However, most of these innovations that have the potential of instigating the modernisation of agricultural activities require high capital investment, which cannot easily be provided by the informal credit sectors such as friends, money lenders and so on. Income obtained by subsistent farmers from both on-farm and off-farm activities is also not adequate for the needed agricultural transition or growth. As a result, most of these farmers grow crops and rear animals on smaller scales due to their financial constraints.

Credit contributes to accelerating the agricultural development provided it is adequate, cheap and development oriented [29]. If credit is found to be adequate and productive, it would enable optimum use of resources and fuller application of improved technology [30]. According to Khandker, traditional agriculture will have low level of production unless supported by reasonable amount of agricultural credit required to purchase different inputs like improved seeds, fertilizers, oxen, pesticides, herbicides, and others. Access to credit promoted the adoption of yield-enhancing technologies and governments used credit programs to promote agricultural output.

Despite the importance of agriculture described in the preceding text and the numerous Asian case studies that support them, there is doubt about whether agriculture can successfully generate enough growth in Africa today [31, 32, 33]. In many respects, this doubt harks back to the immediate post-independence industrialisation policies of many low-income countries, including countries in Africa. At that time, priority was given to heavily subsidised and protected industries, while agriculture was penalised and plundered through unfavourable macroeconomic, trade, tax, and pricing policies. However, scholars such as [26] and [27] remain resolute on the importance of agriculture to development.

The study conceptualises the impact chain model presented in Figure 1. The model principally indicates that interventions lead to changes and modifications on one’s behaviour. As a concept of the study, credit from either institutional or non-institutional sources is intended to serve as an intervention that will assist operators of microenterprises to raise some level of capital in order to expand their businesses or farms. The impact chain model employs two groups in its analysis as adapted by the study. There are two groups of agents where one is given a treatment and the other not. The expectation is that the experimental group would exhibit a favourable outcome as against the control group. The outcome is therefore regarded as the impact of the intervention. In the case of the study, two groups of farmers, that is, farmers with and farmers without credit were chosen. The expectation therefore was that farmers with credit based on the intervention would give a favourable modified outcome as against farmers without credit.

Download as

Download as

3. Methodology

The study employed the quasi-experimental design and a cross-sectional survey design. It used the ‘with and without’ method in assessing the effects of microcredit on the production levels small scale farmers in the Nkoranza North district [34]. A sample size of 152 respondents (experimental group i.e. farmers who had accessed credit) was determined for the study. This assumed a 5 percent margin of error or 95 percent confidence in the results. In order to strengthen the results from the study, another sample size of 152 farmers were selected from the control group (farmers who had not accessed credit). The simple random method was used to select farmers with credit and farmers without credit. These numbers were proportionately distributed among the various farmer groupings in the selected communities in order to ensure fairness in the distribution.

In addition, individuals which included Agriculture Extension Officers, the Loans Officer of the Fiagya Rural Bank, the District Finance Officer and the moneylenders were purposively selected as key informants. They were selected because they were considered to be experts in the field whose special knowledge was beneficial to the study. Interview guide and interview schedule were principally used to collect information from respondents. A pre-test was carried out at Fiema also in the Nkoranza North District. As part of the analysis, Statistical Product and Service Solutions (SPSS Version 16), Microsoft Excel (2007) and the Microfit (MFIT Version 4) were used to generate frequencies, percentages, charts as well as processing the Cobb-Dauglas production function. The independent samples t-test was used to assess the effects of credit on the acquisition of inputs and application of technology. The Cobb-Douglas production function was adopted to find the differences in output of both groups. The results are presented in the next section.

4. Empirical Evidence

Evidence from Table 1 shows that out of the total respondents of 152 farmers with credit, males constituted 78.9 percent as against 21.1 percent of females. Among farmers without credit 86.2 percent of males were selected for the study while 13.8 percent of female responded in the group. The finding confirms the report released by [18] that there is inadequate gender mainstreaming in the field of agriculture.

A greater proportion (37.1%) of the respondents in terms of age was within the 41-50 years. The mean age for the respondents was 42.5 years. In terms of education majority of the respondents, 63.8 percent, indicated that they had not received formal education while 36.2 percent indicated that they had had received various levels of formal education. It can be noted from Table 1 that 33 percent of respondents had worked on their own from 11 to 15 years. A total of 29 percent and 27 percent had had 16 to 20 and above 20 years respectively. Again, eight percent of respondents had farmed between six to 10 years and three percent had farmed for at most five years. The information stated reveals that respondents were very experienced especially when 89 percent of them had farmed between 11 and 20 years. The [18] indicated that most farmers in Ghana are aged.

4.1. Farmers’ Acquisition of CreditThis section reports on the number of times respondents received credit, sources from where they took the credits, forms the loans took as well as how the loans were used. It also considers training farmers had before loans were given to them and how loans were repaid. Respondents for the study had taken credit at different times. In all, 49.3 percent of respondents, that is, farmers with credit had taken credit four consecutive times. Also, 30.9 percent had taken three consecutive times. The remaining 19.8 percent had taken credit five times as presented in Figure 2. The mean amount taken especially in the last three years were GH¢700 (2008), GH¢830 (2009) and GH¢1200 (2010). Figure 2 represents the amount taken as loans in the last three years by farmers with credit. The loans officer mentioned that the bank was unable to give huge loans to farmers because of hire risk level.

Download as

Download as

Farmers with credit obtained credit from different sources. This is presented in Table 2. From Table 2, respondents obtained credit from only four sources namely, the bank, microfinance institutions, moneylenders and friends and relatives. A closer look at the table revealed that more of the respondents (37.5%) obtained their credit from friends and relatives. Comparatively, another source from where farmers obtained credit was microfinance institutions as presented in the table. All the sources seem to attract more clients and it appears they are all vibrant in the credit business in the study area. An observation the table reveals that more farmers obtained credit from all the sources.

The findings from Table 2 supports the assertion by [23] that credit is obtained from both institutional sources such as banks and non-institutional sources such as moneylenders and relatives. The finding also confirms the assertion by Nasir (as cited by [35]) that two-thirds of total credit come from the informal sector and that non-institutional credit is more wide-spread in rural areas. The district finance officer had indicated that the district assembly offered loans to people through the Microfinance and Small Loans Centre (MASLOC). However, it was revealed that none of the respondents had obtained credit from the district assembly source.

Credits obtained by respondents took mainly two forms namely, cash and kind. It was realised that 96 percent of credits acquired by respondents was in a form of cash. And the four percent of their credit was in kind. An analysis of the data also revealed that over 91 percent of respondents did not know the interest rates they paid on their loans. This could be attributed to the high illiteracy among farmers. Only 8.6 percent indicated that they knew the interest on their loans. The finding confirms the assertion by the loans officer that the bank has been assisting farmers both in cash and in kind.

The credits acquired by respondents were put to a number of uses. It can be observed from Figure 3 that 51.3 percent of respondents used their loans to enhance agriculture which constituted mainly the purchasing of fertilizers, insecticides, and herbicide, hiring of labour and acquiring more farm lands. Another 21.7 percent of the respondents used part of their loans to pay school fees. Also, 20.4 percent of the respondents spent part of their loans on other things such as purchasing of home appliances, marriage, building houses and on food items such as rice and meat or fish. Almost six percent of them spent part of their loans on funerals, while 0.7 percent used their moneys to settle hospital bills. The loans officer confirmed that apart from the inputs purchased by farmers, they used part of their loans to buy consumer goods.

Download as

Download as

The findings from Figure 3 confirm a study by [6, 30] that agricultural credit is not only needed for farming purposes but also for family and consumption expenses, especially during the off season. Respondents were asked whether they were given any form of training before the loans were disbursed to them. Almost 93 percent of respondents indicated that they were not trained before loans were given. However, 7.2 percent indicated they were trained before loans were given to them. The lower training level was corroborated by the loans officer who indicated that the bank offered informal training to few customers.

4.2. Effects of Credit on Input AcquisitionThis section assesses how credit affects the acquisition of inputs by respondents. The effect on the input was measured in changes in capital, hired labour, household labour, size of farm and quality of seeds used. It sought to measure whether there is a significant difference between farm inputs used by farmers with credit and farmers without credit. A five-point Likert scale item format was used to assess the poverty indicators of the farmers. The following values were assigned to the responses: 1 represented ‘weak agreement’, and 5 represented ‘strong agreement’ on a scale of 1 to 5. The independent sample t-test was used to find out whether there were any statistically difference between farm inputs used by farmers with credit and farmers without credit at 0.05 significance level. Table 3 shows the results of the test.

From Table 3, it is discernible that all the items measuring farm input showed significance differences between farmers with credit and farmers without credit. In the case of capital, farmers with credit had a mean capital of 605.8 as against a mean of capital of 452.6 for famers with credit. This means that farmers with credit used more capital than farmers without credit [2]. This was not different from the dependence on hired labour as farmers with credit had a higher mean of 214 as against a mean labour of almost 203 for farmers without credit. The conclusion therefore was that farmers with credit hired more labour than farmers without credit. This supports a study by [36].

In a sharp contrast, farmers without credit employed more household labour than farmers with credit. From the table, farmers without credit had a mean of 153.15 while farmers with credit had 102.83. The finding was confirmed by the extension officers that farmers who were beneficiaries of credit employed more labour than farmers who did not take credit.

From the table, there was a statistically significant difference between the size of farm cultivated by farmers with credit and farmers without credit. The difference was in favour of farmers with credit because farmers with credit had a mean farm size of 0.14 hectares as against 0.11 hectares cultivated by farmers without credit. Based on the analysis given, it can be concluded that farmers with credit used more farm inputs than farmers without credit. This supports the finding by [37]. Kidane indicated that credit positively affects the acquisition of large farm size. The extension officers, the moneylenders also supported this finding.

4.3. Effects of Credit on Technology ApplicationThis analysis examines the impact of credit on farmers’ application of technology. It answers the hypothesis: There is a statistical difference between technology applied by farmers with credit and farmers without credit. Farmers do not only use farm inputs but apply technology as well. This enables them to increase productivity. The respondents for the study applied inorganic fertilizer and herbicides. They also used various varieties of seeds and applied different methods of sowing seeds. The independent samples t-test was used to compare the means of the various technologies applied by the respondents. The test was run at 95 percent confidence level and an alpha level of 0.05.

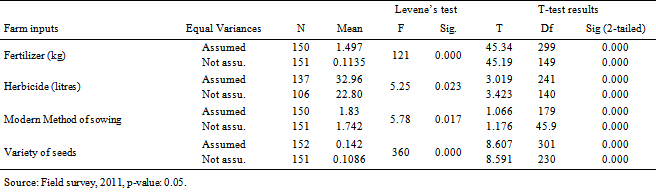

It is observed from Table 4 that farmers with credit obtained a mean of almost 1.5 as opposed to 0.1 obtained by farmers without credit. The F-test for fertilizer was 121 and was statistically significant at 0.000, less than the alpha of 0.05. The t-value of 45.19 was chosen and was statistically significant at 0.000 in the 2-tailed test. It can therefore be concluded that farmers with credit applied more fertilizer than farmers without credit. The result confirms the study by [38] that access to credit increases the use of inorganic fertilizer. The finding was supported by the extension officers who asserted that farmers who take credit are able to buy and apply more fertilizer.

In the case of herbicide, farmers with credit had a mean of almost 33 as against 23 obtained by farmers without credit. The Levene’s F-test was 5.25 and was statistically significant. The equal variance assumed t-value of 3.423 was adopted and was also statistically significant because it was less than the 0.05 alpha. This indicates that farmers with credit applied more herbicides than farmers without credit.

An examination of Table 4 proves that farmers with credit applied more modern methods of sowing seeds and used more modern varieties of seeds. One of the methods used by farmers with credit was line sowing with the help of ropes and machines. The varieties of seeds used included dobidi, coupon, obaatanpa, abrontia and Atiaa. In contrast, farmers without credit used less of those methods and varieties. The reason was that farmers with credit obtained higher means in these variables as compared with farmers without credit. The t-values in the two variables were all significant in the 2-tailed test hence the conclusion. The information provided by the extension officers support this finding. They confirm the assertion that credit beneficiaries buy and use new varieties of maize seeds compared to non-beneficiaries.

The data in Table 4 show that there was statistically significant difference between the technologies applied by farmers with credit and farmers without credit. The data indicate that, farmers with credit acquired higher means compared to farmers without credit. It can therefore be concluded that farmers with credit applied more technology than farmers without credit. The finding confirms the study by [39] that the use of modern technology increased demand for credit and resulted in increase in agricultural productivity of small farmers. The model of impact chain proposed a possible influence of credit on farmers’ adoption of technology. The finding indicates the positive side of the model, in the sense that credit has affected the adoption of technology by farmers.

Respondents were asked about how they obtained their seeds and their responses have been presented in Figure 4. From the figure, 66.9 percent of respondents of farmers with credit indicated that they obtained seeds from their own farms; four percent obtained their seeds from Ministry of Food and Agriculture (MoFA) and 29.1 percent obtained seeds from the open market. However, 75.7 percent of respondents among farmers without credit obtained seeds from their farms, and 24.3 percent got their seeds from the open market. No farmer obtained credit from the ministry in charge of agriculture. If majority of respondents obtained seeds from their farms then it presupposes that farmers may not be using certified, approved and disease resistant seeds. This view was shared by the extension officers who added that most farmers refuse to heed to directions given by agriculture extension officers.

Download as

Download as

5. Conclusion and Policy Recommendations

Based on the findings from the study, it can be concluded that with credit, farmers are able to acquire additional farmlands and other farm inputs like capital, seeds, and agro-chemicals (fertilizer and herbicide). The acquisition of these inputs for farming purposes in turn causes increased output which is the aim of every farmer. However, credit beneficiaries did not use all the credit they acquired to enhance agricultural output and this might have affected the full realisation of the benefits of credit. Credit enables farmers to adopt more technology in their farming business. The acquisition of agricultural technology such as the application of fertilizer, employing of modern methods of farming and cultivation of modern varieties of seeds is the right course to ensure increased output. Technology is necessary for transforming the peasant and subsistence agriculture in Ghana.

Farmers in the study area must consider acquiring more credits in order to transform their agricultural activities from peasant and subsistence agriculture to commercial agriculture. This is because credit enables farmers to purchase more inputs and apply more technology. Farmers must use the credit they acquire for its intended purposes. This will enable them to increase their output and avert loan default. Since farmers without credit were in need of fertilizers and modern varieties of seeds which required huge sums of money it is recommended that they should consider joining the farmers associations in their communities which would facilitate their access to credit.

References

| [1] | M. Duvendack, R. Palmer-Jones, J.G. Copestake, L. Hooper, Y. Loke, and N. Rao, What is the evidence of the impact of microfinance on the well-being of poor people?, Centre, Social Science Research Unit, Institute of Education, University of London, London, 2011. | ||

In article In article | PubMed | ||

| [2] | M. Otero, Bring development back into microfinance, University of Frankfurt, Goethe, 1999. | ||

| In article | |||

| [3] | Nosiru, Micro credits and agricultural productivity in Ogun State, Nigeria. World Journal of Agricultural Sciences, 6(3), 2010, 290-296. | ||

| In article | |||

| [4] | International Finance Corporation, IFC, GAFSP $10 million in root capital to support small farmers in Africa, Latin America, World Bank Group, Washington D.C., 2011. | ||

| In article | |||

| [5] | World Bank, Agricultural growth for the poor: An agenda for, World Bank, Washington D.C., 2009. | ||

| In article | |||

| [6] | R. Burgess, and R. Pande, Do rural banks matter? Evidence from Indian social banking experiment. American Economic Review, 95, 2005, 780-95. | ||

| In article | View Article | ||

| [7] | N. S. Parthasaraty, Assistance in Institutional Strengthening and Agricultural Policy. Final report on agricultural credit, Damascus. 2001, October. | ||

| In article | |||

| [8] | D. Hulme, Impact assessment methodologies for microfinance: A review. A paper prepared for the virtual meeting of CGAP Working Group on Impact Assessment Methodologies, Word Bank, Washington D.C., 1997. | ||

| In article | |||

| [9] | F. I. Olagunju and R, Adeyemo, Agricultural credit and production efficiency of small-scale farmers in South-Eastern Nigeria. Agricultural Journal, 2(3), 2007, 426-433. | ||

| In article | |||

| [10] | D. Zerfu and D.F. Larson, Incomplete markets and fertilizer use: Evidence from Ethiopia, policy research working paper 5235, The World Bank, Washington D.C., 2010. | ||

| In article | |||

| [11] | F. Enu-Kwesi, F. Koomson and R. Baah-Mintah,The contribution of Kakum Rural Bank to poverty reduction in the Komenda-Edina-Eguafo-Abrem Municipality in the Central Region, Ghana. Economic Annals, 58(197), 2013, 121-140. | ||

| In article | View Article | ||

| [12] | Ghana Statistical Service, National account statistics: Revised gross domestic product 2011, Ghana Statistical Service, Accra:, 2012. | ||

| In article | |||

| [13] | P. Asiama and V. Osei, Microfinance in Ghana: An overview, Bank of Ghana: Economic Web Institute, Accra, 2007. | ||

| In article | |||

| [14] | T.E. Anin, Banking in Ghana, Woeli Publishing Services, Accra, 2000). | ||

| In article | |||

| [15] | Association of Rural Banks, First quarter (2009) report on the performance of rural and community banks (RCBs), Efficiency and Monitoring Unit, Accra 2009. | ||

| In article | |||

| [16] | World Bank, Implementation completion and results report on IDA credit and IFAD loan to the Republic of Ghana, World Bank, Washington D.C., 2009. | ||

| In article | |||

| [17] | Bank of Ghana (2012). Register of rural and community banks as of March 2012. Retrieved from: http://www.bog.gov.gh/index.php? option=com_ content&view=article&id=83&Itemid=125. | ||

| In article | |||

| [18] | Ministry of Food and Agriculture, Food and agriculture sector development policy II. (Accra: MoFA, 2007). | ||

| In article | |||

| [19] | Food and Agriculture Organisation (2004). Food balance sheet, Ghana 1961-2002, Retrieved on 9th October, 2014 from www.faostat.fao.org. | ||

| In article | |||

| [20] | Ministry of Food and Agriculture, Agriculture in Ghana: Facts and figures, Statistics, Research and Information Directorate, MoFA, Accra, 2001). | ||

| In article | |||

| [21] | J.A. Afolabi, Analysis of loan repayment among small scale farmers in Oyo State, Nigeria, Journal of Social Sciences, 22(2), 2010, 115-119. | ||

| In article | |||

| [22] | Ghana Statistical Service, Ghana living standard survey on the fifth round (GLSS 5), Ghana Statistical Service, Accra, 2007. | ||

| In article | |||

| [23] | J. H. Owusu-Acheampong, Rural credit and rural development in Ghana, in C. K. Brown, (Ed.), Rural Development in Ghana, Ghana University Press, Accra 1986. | ||

| In article | |||

| [24] | Tsogbe, E. Y. (2002). Micro credit, agricultural output and food security – African advocacy forum II. Microcredit – Solution for Africa United Nation New York: Retrieved on January 13, 2011 from www.un.org/esa/africa/ microfinace_model.pdf. | ||

| In article | |||

| [25] | M. Yunus, Expanding microcredit outreach to reach the millennium development goals, International Seminar on Attacking Poverty with Microcredit, Dhaka. 2003 | ||

| In article | |||

| [26] | D. Cervantes- Godoy, and J. Dewbre, Economic importance of agriculture for poverty reduction. OECD Food, Agriculture and Fisheries Working Paper, No. 23, OECD Publishing, Washington D.C., 2010. | ||

| In article | |||

| [27] | X. Diao, P. Hazell, D. Resnick, and J. Thurlow, The role of agriculture iin development: Implication for sub-Saharan Africa. Research report 153, IFPRI, Washington D.C, 2007. | ||

| In article | |||

| [28] | N. Abedullah, M., Mahmood, M. Khalid, and S. Kouser, The role of agricultural credit in the growth of livestock sector: A case study of Faisaland, Pakistan Veterinary Journal, 29(2), 2009, 81-84. | ||

| In article | |||

| [29] | I.O. Badiru, Review of small farmer access to agricultural credit in Nigeria. Policy Note 25, International Food Policy Research Program, Rome, 2010. | ||

| In article | |||

| [30] | S.R. Khander, Fighting poverty with microcredit: Experience of the Grameen Bank and other programmes in Bangladesh, World Bank, Washington D.C., 2006. | ||

| In article | |||

| [31] | P. Coilier, Primary commodity dependence and Africa’s future, in B. Pleskovic (Ed.), Annual World Bank conference on development economics proceedings, World Bank, Washington D.C., 2002. domestic product 2011. Retrieved from: http://www.statsghana.gov.gh/docfiles/GDP/revised_gdp_2011_april-2012.pdf | ||

| In article | |||

| [32] | F. Ellis, Small farm, livelihood diversification, and rural-urban transitions: Strategic issues in sub-Saharan Africa. Paper presented at the Future of Small Farms, Research Workshop, Wye, U.K., 2005, 26th- 29th June. | ||

| In article | |||

| [33] | S. Maxwell, and R. Slater, Food policy old and new. Development Policy Review, 21(5), 2003, 531-553. | ||

| In article | View Article | ||

| [34] | A. Rubin, and E. Babbie, Research method for social work (7th ed.), Brooks/Cole, Belmont 2008. | ||

| In article | |||

| [35] | M.K. Bashiir, Y. Mehmood, and S. Hassan, Impact of agricultural credit on productivity of wheat crop: Evidence from Lahore, Punjab, Pakistan. Pakistan Journal of Agricultural Science, 47(4), 2010, 405-409. | ||

| In article | |||

| [36] | A. Belete, M. B. Masuku, M, and P. Mavimbela, Contribution of savings and credit co-operatives to food crop production in Swaziland: A case study of smallholder farmers. African Journal of Agricultural Research, 5(21), 2010, 2868-2874. | ||

| In article | |||

| [37] | A. T. Kidane, Impact and implications of agricultural credit use on gross farm income in southern Ethiopia, masters diss., Norwegian University of Life, Norway, 2007. | ||

| In article | |||

| [38] | T. Matsumoto, and T. Yamano, The impact of fertilizer credit on crop production and income in Ethiopia. Discussion paper, 2010, 10-23. | ||

| In article | |||

| [39] | A. Saboor, H. Maqsood, and M. Madiha, M, Impact of micro credit in alleviating poverty: An Insight from rural Rawalpindi, Pakistan. Pakistani Journal for Life and Social Science, 7(1), 2009, 90-97. | ||

| In article | |||

CiteULike

CiteULike Delicious

Delicious

){kind=link}

{kind=link}

){kind=link}

{kind=link}

){kind=link}

{kind=link}

){kind=link}

{kind=link}